THE WEEKLY TOP 10....The risk/reward equation has changed significantly

THE WEEKLY TOP 10

Table of Contents:

1) Is all of the good news already priced into the mega-cap techs over the near-term?

2) Some of the obvious froth in the market place is becoming ridiculous.

3) High yield is trying to breakout. If it can, it will be bullish for stocks as well!

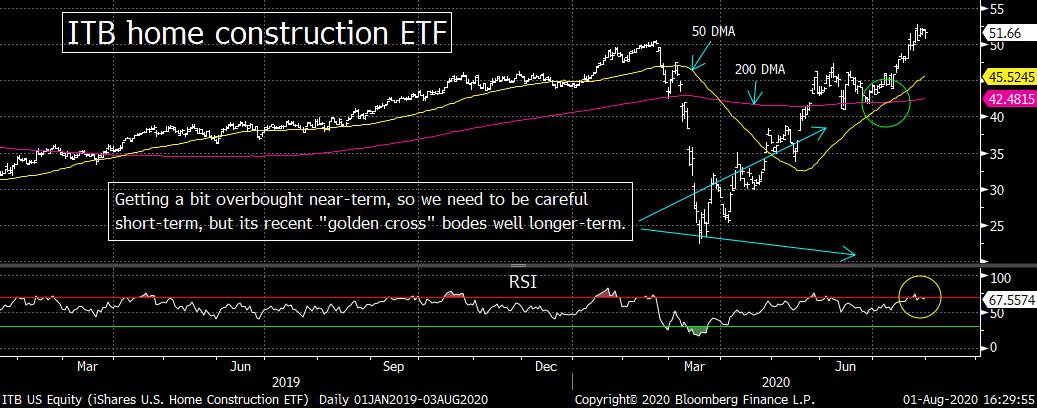

4) The housing stocks are a bit overbought, but still look great longer-term.

4a) Expect the migration out of the cities and into the suburbs to continue in 2021.

5) U.S. Treasuries yields fall to new historic lows.......Hello????????

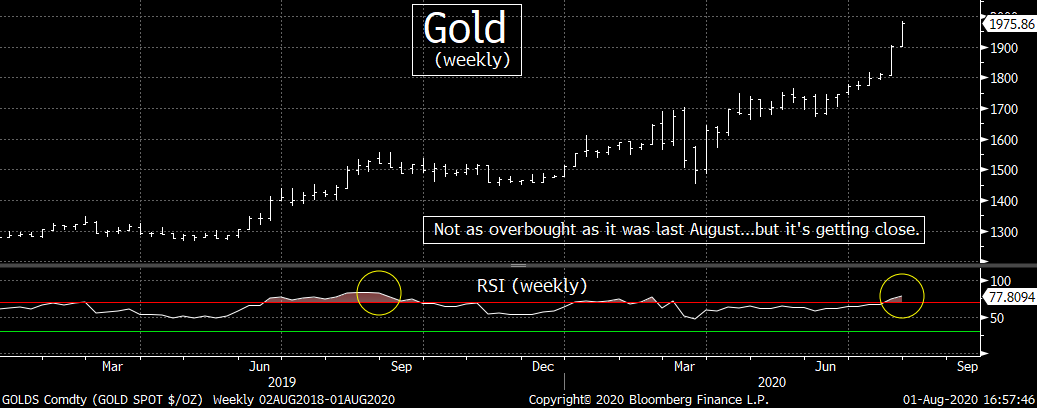

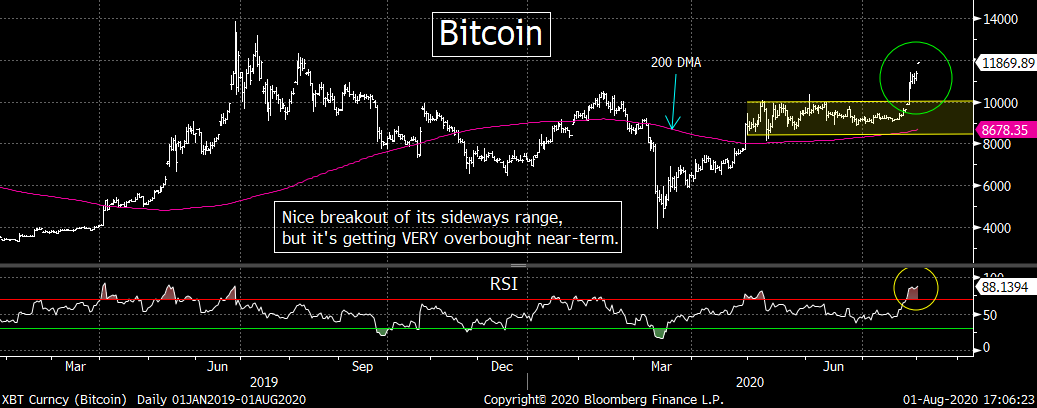

6) Gold is overbought...and so is Bitcoin...but we’re bulls longer-term on both.

7) Starting to see a few cracks in several European markets.

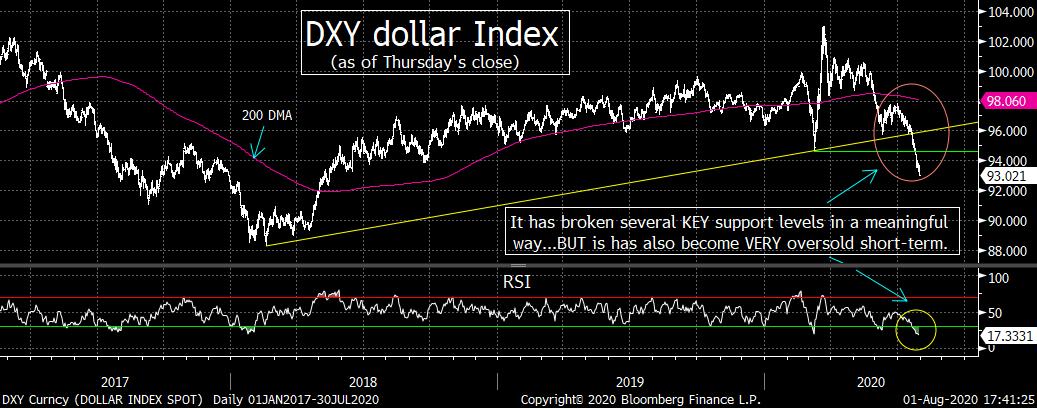

8) The dollar is VERY oversold, but any bounce might be short-lived.

9) Once Biden picks his VP candidate, the campaign can FINALLY begin.

10) Summary of our current stance.

Short Version:

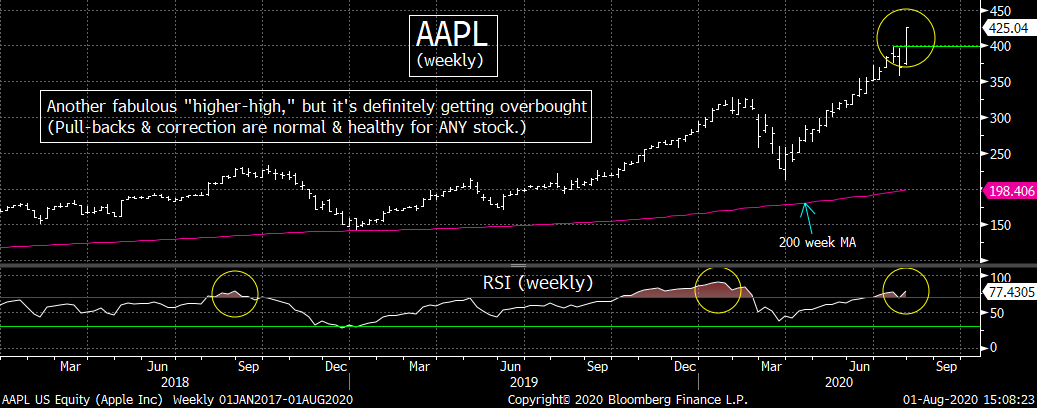

1) The mega-cap techs stocks have reported great earnings. However, they have also seen GREAT rallies...that have taken them to overbought levels...and overvalued levels. So as great as these companies are, their stocks have still become vulnerable to significant declines right now...even if they’re headed a lot further longer-term. Tech stocks ALWAYS see a lot of BIG swings...in BOTH directions...that’s what they do!

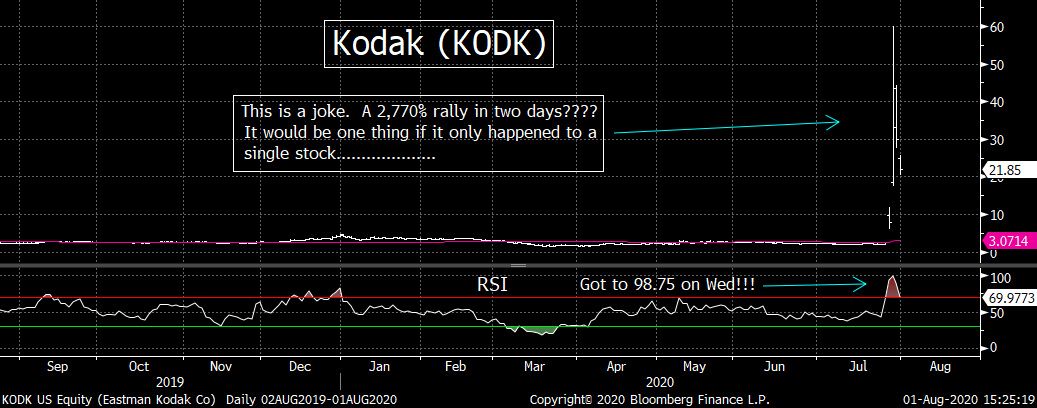

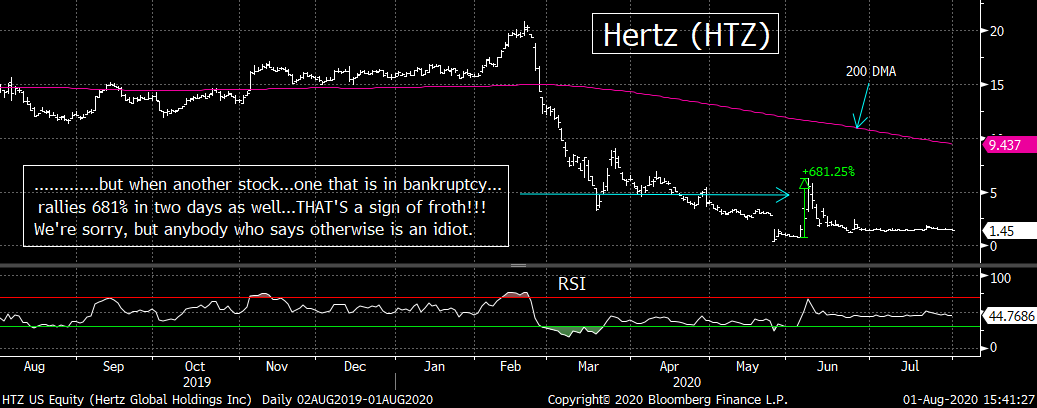

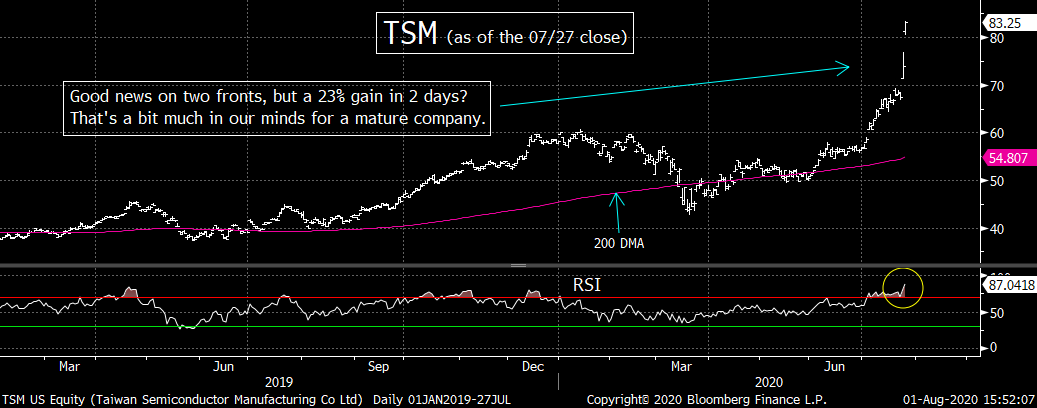

2) The froth that has shown up in the stock market recently has become ridiculous. No, it’s not as extreme as it was in 1999/2000, but it IS still there. Anybody who thinks the recent action in stocks like Kodak and Hertz are not obvious signs of froth are idiots.....”Froth” is not always followed immediately by corrections, but we’d also note that we’re not just seeing it is down-and-out companies. There are signs of it in stocks like TSLA and TSM as well.

3) On the positive side of the ledger, the high yield market continues to act well. It is getting a bit overbought, so it might need to take a “breather” soon, but if the HYG can break above its 200 DMA in a more meaningful way (either now...or after a breather), it’s going to be a very bullish development for this asset class. Since high yield has been a leading indicator for stocks in the past, a breakout in the HYG would be bullish for stocks as well.

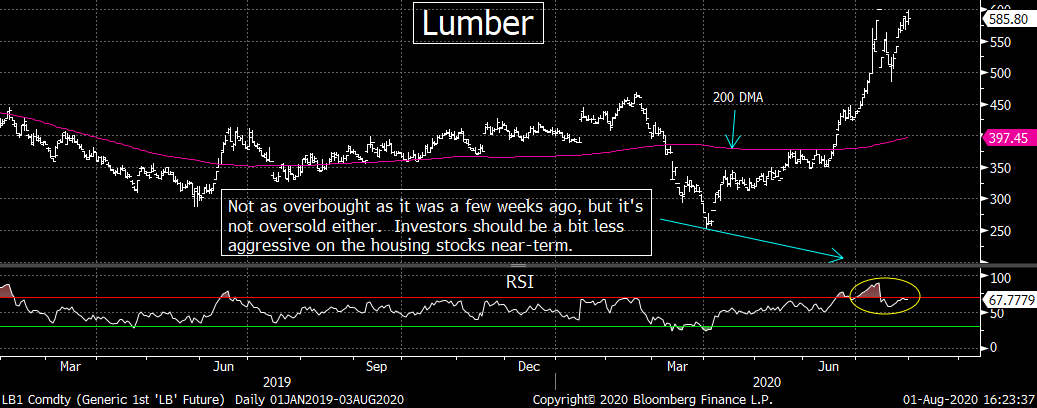

4) Staying on the positive side of the ledger, the housing stocks continue to act very well. Lumber did pull-back from its extremely overbought condition, but it did that very quickly...and it has begun to bounce back again already. The ITB home construction ETF has become overbought, so it still might need to take a further breather, but any meaningful move above its July highs will confirm that the strong rally in this group still has further to go.

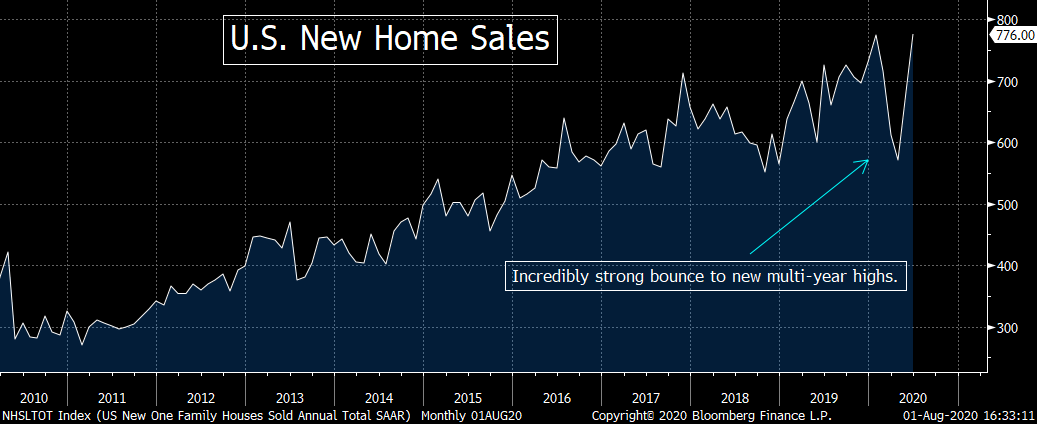

4a) We’d also note that the data on Housing Starts and New Home Sales continues to be impressive. It is our belief...based on what we’re seeing in the southern hemisphere (where it’s winter time) in terms of bigger “second waves” of Covid-19...that the migration out of the cities and into the suburbs will continue through 2021.

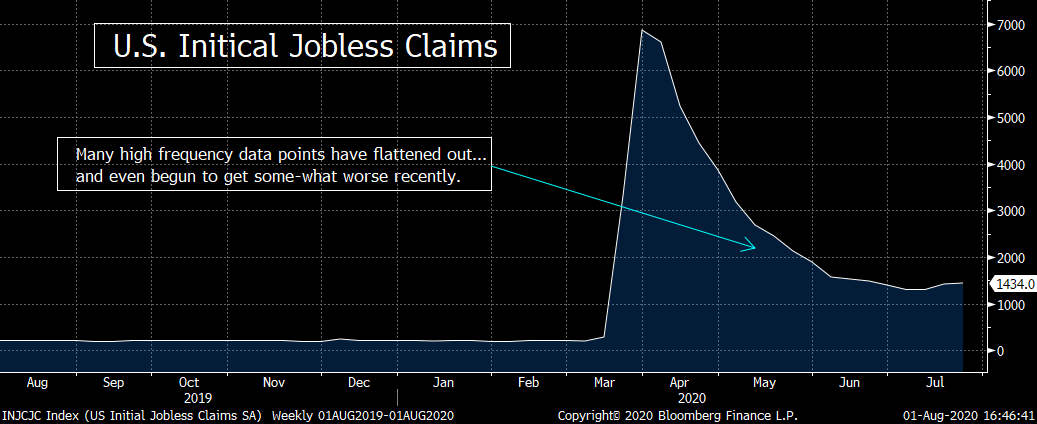

5) The yield on the U.S. 10-year Treasury note closed at an all-time low on Friday (as did other yields at different maturities). We know how some pundits keep trying to explain this away, but when you combine these moves with the slowing high frequency data...and it shows that the Treasury market is indeed sending the stock market another warning signal about the pandemic (just like it did in January and the first half of February).

6) Speaking of warning signals, gold is sending up one as well. That said, it is getting quite overbought, so the $2,000 level should provide some very tough resistance over the near-term. With this in mind, we think investors should be much less aggressive up at these levels over the near-term.......Bitcoin is even more overbought, so it should be due for a short-term pull-back as well. However, the fact that it broke significantly above $10,000 should be very bullish for the cryptocurrency on an intermediate-term basis...especially since it is such a momentum-driven asset class.

7) We have been quite bullish on Europe...especially Germany recently. However, its markets are showing some cracks...with the German bund yield rollikng over again...and the DAX index breaking a couple of support levels. It will take more of a decline for us to send up any warning flags, but it’s something we’ll be keeping a close eye on over the coming days and weeks. This is especially true since the European banks stocks are looking a bit dicey once again.

8) We’ve seen some serious technical damage done to the DXY dollar index over the past two weeks. It has become very oversold on a near-term basis, so it should see a bounce next week (following its strong pop on Friday). However, if it breaks below its lows from last Thursday in any meaningful fashion over the coming weeks and months, it will confirm a SIGNIFICANT change in trend for the greenback...which will have important implications on several economic (and political) fronts.

9) It looks like Vice President Biden is going to put-off his VP selection until the second week in August. Whenever the pick is made public, the real campaign will FINALLY begin!......We have attached a very interesting article about why one person thinks President Trump should drop out of the election. This has NOTHING to do with what we think SHOULD happen (and we certainly don’t think that it WILL happen), but it is still a very intriguing and thought provoking article. We hope you’ll take a few minutes to check it out.

10) Summary of our current stance. We believe the stock market is setting up for a pull-back or even a correction in August. In fact, given what we’ve seen in the markets recently, the bulls should be HOPING for a correction. Healthy markets do not see the kind of froth that we have seen in recent weeks...especially when this froth comes at a time when valuations are extended...and when other markets are sending up warning signals. A correction would take some of this froth out of the market place...and give the stock market a better chance to rally further in the future. If it continues to rally in a substantial way, we’ll be looking at a third bubble...and then a third disastrous bear market...within one single generation.

Long Version:

1) Over the near-term, the most important action in the stock market should continue to be in the mega-cap tech stocks. This may seem like an obvious statement, but after the huge moves they experienced over the past few months...and now that they’ve all reported earnings...how they act over the next week or two should be very important for the broad stock market.

For the most part, these companies (FB, AMZN, AAPL, NFLX, GOOGL, TLSA, MSFT, NVDA) reported very good earnings. Yes, NFLX, TLSA and GOOGL are down 11%, 5% and 12% from their all-time highs, but they still remain 63%, 40% and 354% above their March lows! (As for the other five, FB, AAPL, AMZN, MSFT and NVDA remain 72%, 89%, 88%, 50% and 115% above their March lows respectively.)......As for valuations, they trade at anywhere from 28x projected earnings to 184x (and 31x and 613x stated earnings). Of course, valuations are a HORRIBLE timing tool, but there is no question that most of these names are at...or very close to...the top-end of their historical valuation ranges.

The reason we highlight these basic statistics revolves around a very simple question: What next??? In other words, with these stocks getting (even more) expensive...and have rallied in such a powerful manner over the past four months...and have all become quite overbought on a near-term basis...we have to wonder if these stocks can rally a lot more...even though they have just reported some positive fundamental news.

On the one hand, FB & AAPL were able to close at new all-time highs on Friday, but on the other hand, TSLA, MSFT and AMZN all closed below the opening levels that they produced the morning after they reported. AMZN closed only 2.5% below its highs, but for the third time in July, the stock tested 3,200 on an intraday basis, but was not able to close above that level. So it’s action was still some-what disappointing.

What we’re really trying to say is that our over 30 years of experience on Wall Street tells us that when a stock or a group of stocks experience a great run over a short-period of time (and thus become overbought)...and then they report some very good news (thus leaving them with nothing more positive to say for at least a little while).....they sometimes become vulnerable to a pull-back (sometimes material ones). Therefore, how these mega-cap stocks do over the next two weeks could/should continue to be very, very important.

For us...as we highlighted on Friday in our daily “Morning Comment” piece, we actually hope that these names do indeed pull-back. In fact, we hope they see pretty significant corrections. It would put some fear back into the market...and take some complacency out of it as well. Heck, AAPL could fall 20% and still remain above its old record highs from February!!! So a meaningful pull-back in these names would take some froth out of the market...without causing any real damage. In fact, it would be healthy.

2) Speaking of froth, the move we saw last week in Kodak was ridiculous!!! Remember when this great old photographic film company was going to become a cryptocurrency company a few years ago (when bitcoin was trading above $19,000?). Well, it looks like they’re now going to become a pharmaceutical company!!! Wow, we thought it was great when Corning (GLW) went from a cooking pot company...to one that made the screens for computers and smart phones, but to be able to make a shift like Kodak has made...TWO TIMES in less than three years...is amazing!!!

When cryptocurrency “shift” made the rounds in early 2018, the shares of Kodak rallied 335% in just two days (on an intraday basis). However, that PALES in comparison to the 2,716% rally it saw over two days this past week...now that it has become a pharma company!!!......We would argue that a big part of this move has been due to the Robinhood investor...and the impact they are having on individual names right now. On top of the crazy move in Kodak last week (which fell from $60 down to $21 by Friday’s close)....we have also seen crazy moves in Hertz...when the bankrupt company rallied 681% in just two days on an intraday basis back in June. And who can forget when Tiziana Life Sciences (whose ADRs have the symbol TLSA) was mistaken for a company that was associated with Telsa (TSLA) and sored 283%.

The examples of froth don’t just come from some down and out companies. Just look what happened to Taiwan Semiconductor (TSM). It rallied 23% in the two days after it reported earnings a week and a half ago. Yes, TSM’s earnings WERE great...and the negative news about INTC was certainly bullish for them, but this is a mature company...and it’s not like they just discovered the vaccine for Covid-19! Therefore, a 23% rally (after it had already rallied 53% over just three months) seemed extreme in our minds. This is especially true given that it took its P/E ratio above 30x its estimated earnings...and took its RSI chart up near 90. Therefore, we think this is another example of how things are getting a bit out of control...and thus frothy.

There is no question that there were a lot more examples of these kinds of moves back in the 1990s. However, as we’ve said a zillion times before, we will never see another bubble like the one we saw in the late 1990s in our life times....and we do not have to see THOSE kinds of extremes to declare that the market has become extended and “frothy.”........This does not mean that the stock market HAS to see a decline right now. Like high valuations, froth can last for a long period of time. However, anybody who thinks these examples are not signs of froth in the market place is an idiot.

3) On the positive side of things, by definition, if somebody says a market is getting frothy, it HAS to be acting well, so we cannot say with certainty that a reversal will happen immediately. The Nasdaq Composite closed within a whisker of its July 20th record highs...and it did give us a new closing high on a weekly basis...and its third record closing high in a row on a monthly basis! The S&P 500 also finished the week within a whisker of its July 22ndhighs...and above the sideways range we had been harping on for many weeks. (It’s still not enough of a break to confirm a breakout, but the action has still been quite good...duh.)

However, maybe the best news of the past few weeks has been the action out of the high yield market. The HYG high yield ETF closed slightly above its June highs last week and is now starting to pull-away from its 200 DMA...which has provided tough resistance since that market broke down in the first quarter. The HYG is starting to get overbought, but if (repeat, IF) the HYG can pull further away from its 200 DMA (whether now or after a short “breather”)...and thus move it meaningfully above the sideways range it has been in for over two months, it’s going to be bullish for this asset class..........Since the high yield market can frequently be a leading indicator for the stock market, that would be bullish for stocks as well.

In other words, we’ll be watching this ETF very closely going forward. Even if it fails to break above $85 right now, we’ll be watching it on any near-term pull-back. If it is a shallow decline...that is followed by a substantial move above its recent highs....it should signal that any pull-back in the broad market will be follow by another strong rally leg soon.

4) Staying on the positive side of the ledger, one area of the economy which continues to act incredibly well is the housing sector. We have been bullish on this group since the very early part of the recovery from the March lows, but we had also warned that the price of lumber had become incredibly overbought a few weeks ago. Therefore, we said, investors should avoid chasing the homebuilders...and look to buy them on weakness instead.

Well, sure enough, lumber did indeed roll-over in a significant way...as it dropped almost 20% immediately after we made that call. The problem is the 20% decline (on an intraday basis) only took 5 days to playout. That was not long enough to hurt the housing stocks in any material way...and the commodity has already bounced-back to those early July highs! Therefore, even though the decline was a sharp one, it merely worked off the extreme overbought condition...and it did not hurt the housing stocks much at all. No, we never thought that a drop in lumber would clobber the housing stocks, but we did think it could cause them to see at least some kind of a pull-back. We were wrong on that short-term call...and the group continues to look great on a long-term basis...and thus remain bullish on the group over the intermediate-to-long-term.

We do need to point out, however, that although the chart on lumber is not anywhere near as extreme as it was a few weeks ago, it has still moved back up close to an overbought condition once again. More importantly, the ITB home construction ETF is also sitting at a level that is bordering on an overbought condition. Given that we believe a pull-back...or even a correction...in the broad stock market is likely in August, this group could be in for some short-term weakness as well.

Wait a minute, Maley...which is it...are you bullish or bearish on the group???? What I’m trying to say is that I am still quite constructive on the homebuilders, so I am no longer saying that investors should step back from the group and let it come to them. Rather, investors should continue to nibble away at the group at these levels...but they should be a little less aggressive up here...and look to get more aggressive on any weakness.

4a) On a fundamental basis, the housing industry looks great. New home sales have exploded since March (as have pending home sales)...and Housing Starts have increased by over 25%. Mortgage rates continue to make historic lows on almost a daily basis......It is also our opinion that the migration away from cities and towards the suburbs will continue through 2021. New York City is already saying that they will not reopen their schools unless the daily infection rate is below 3%. As we will discuss further in the next point, we’re seeing signs in other parts of the world...who are now in winter...where the waves of Covid-19 are stronger than the first waves. That does not bode well for further waves in the U.S. As city dwellers who have been thinking they will stick it out...are forced to have their families stuck at home through another winter...where they don’t have enough room to co-exist for long periods of time...we’ll see a lot more people make the decision to move out of urban areas.

We’d also like to remind people of one other time in history. Back in the 1970s, inflation was a big problem...and it caused interest rates to skyrocket. We are not in the inflation camp yet, but we certainly understand the reasoning behind the belief that inflation is going to pick-up soon. However, we’d just like to mention that housing prices rose dramatically during the 1970s...even though mortgage rates moved higher. Inflation was great for the housing market...as people felt more comfortable with an asset that they could touch and feel.......Needless to say, the housing market of the 1970s is different than it is today...as is the U.S. economy. However, we just wanted to point out that there are other factors besides interest rates that determine the state of the housing market in the U.S. from time to time.

5) The yield on the 10-year Treasury note closed at an all-time low on Friday of 0.528%...which (by definition) takes it below its March lows. When you combine this with the weakening high frequency data on such things as Open Table, Apple Map hits, airport passenger screening, jobless claims, etc...it sure looks like the rate of growth in the U.S. is going to slow going forward.

To be honest, we believe that the bond market is not just looking at the recent high frequency data. It’s also looking at what’s going on in the southern hemisphere (where it is winter time)...and seeing an even another wave of the pandemic...which will slow the rate of economic growth even more in those parts of the world. Just look what is going on in Melbourne, Australia. They are seeing a second wave that is stronger than the first one back in March...and they are looking at another possible lock-down!!! The reports are that within days, Melbourne will likely implement a tough “stage four” lockdown...that would force some businesses to close, impose stricter stay at home rules and cut public transportation services......Here in this country, we’ve see many areas already experience a second wave, but we haven’t even gotten to the cold weather months yet....where people stay inside a lot more...and thus in closer contact with one another.

Back in January and early February of this year, the Treasury market saw what Covid-19 would do to the economy and it reacted in a significant way...as the yield on the 10yr note fell from 1.8% at the beginning of the year to 1.5% by mid-February...a decline of 18%. (We use February 19 as the end point...because that is when the stock market finally reacted to the pandemic.).....This time around, since early June, the yield on the 10yr note has fallen a whopping 40% (from 0.9% to 0.53%). Even if you start in mid-June, the decline in yields has been more than it was on a percentage basis back at the beginning of the year (it has fallen 28% since mid-June).

A lot of pundits continue to give us several reasons why this decline in Treasury yields is nothing to worry about. However, there is no question that the high frequency data is slowing down on several fronts...and that the coronavirus is seeing another wave in the areas of the world where the weather is colder (something we will face before long). The Fed is there with their safety net, but those who are looking for any further improvement in the economy will almost certainly need a reliable and widely available vaccine very quickly...or they’re going to be sorely disappointed.

6) Of course, the other asset class that forewarned the stock market about the iimpact the pandemic would have on the global economy back in January and the first half of February was gold. The rally in gold has been well documented...and our call that said the breakout above $1,750 would lead to a very quick move to the old 2011 record highs has worked out very, very well.

Ok, now that we’ve separated our shoulders patting ourselves on the back, we want to reiterate something we said early last week in one of our “Morning Comments.” Gold is getting overbought on a short-term basis. In that note a few days ago, we said that the yellow metal could still rally a bit more...as one the charts that was getting overbought was not quite as extreme as it was a year ago (just before the 2019 rally in gold flattened out for a couple of months)...but we believe that the $2,000 level should provide some very tough resistance over the very-short-term.

Longer-term, we still like gold very much. It’s technical breakout to new all-time highs has been an impressive one. Therefore, intermediate-to-long-term investors should sit tight with their holdings...and look to add to them on weakness. Shorter-term traders should think about taking some chips off the table at times when it pops its head above the $2,000 level for now....and look to add to positions after it sees a pull-back (that helps work-off this overbought condition).

We’d also note that Bitcoin broke significantly above its KEY $10,000 resistance level last week...which is very bullish. However it has become VERY overbought on a very-short-term basis, so we would not be chasing it aggressively up here (at the $11,500 level). HOWEVER, there are few assets that are more sensitive to “momentum” than Bitcoin, so we’re NOT saying that people should avoid it completely up at these levels. We’re merely saying they should be a bit less aggressive. We believe any pull-back in Bitcoin will be shorter-lived than any decline we see in gold...now that it has broken above this all-important resistance level. So investors and traders alike do not want to be too passive right now.

One thing is for sure about the technical condition of Bitcoin right now. If any near-term pull-back holds above that old resistance level of $10,000...and an ensuing bounce takes it above whatever “high” it makes in its current move, it’s going to be WILDLY bullish for the cryptocurrency. In other words, if Bitcoin can follow this week’s breakout (above its three month sideways range)...with a “higher-low/higher-high” sequence...the renewed upside momentum in this cryptocurrency should be quite powerful!!!

7) One of the themes we have been harping on for several months has been the outperformance of the European markets since the March lows. More recently, economists have been talking about how the economic rebound in Europe from the impact of the pandemic has been better than in the U.S.....However, we are starting to see a few cracks in this scenario, so it’s something we’re going to be watching very closely over the coming days and weeks.

On the fundamental side of things, we saw some disappointing GDP reports...as Germany, France and Spain all reported lower-than-expected data. Of course, GDP data is backward looking...and we’ve seen a nice rebound in other data points...like their monthly PMI data. (The Markit Eurozone Manufacturing PMI number for May was 51.1...above the all-important 50 level). However, like we’ve seen in the U.S., bond yields have been falling again in Europe since early June...with Germany’s 10yr bund now yielding a negative 0.526%. We’ve seen similar declines in yields across the continent, so there is no question that there is fear in their credit markets that things will slow as we move through the second half of the summer.

We’d also note that the most important stock market in Europe has been under some pressure over the past week and a half...as Germany’s DAX has decline 6%...and has fallen slightly below its trend-line from the March lows. This is NOT a big warning flag by any means. The DAX had become overbought on a short-term basis, so it was due for a bit of a pull-back anyway. So we don’t want to make too much of this development just yet...but we don’t want to ignore it either.

The DAX remains above its 200 DMA, so that is positive. If it breaks below that line, however, it WILL raise some more compelling concerns in our minds. This would be particularly true because not only has the DAX broken below its trend-line from March, but it has also broken below an “rising wedge” pattern. A break below the 200 DMA (of 12,207) would raise a yellow warning flag...and a meaningful move below its mid-June lows (of 11,900) would turn it into a red one.

We’ll also be watching the European banks very closely (much like we always do). This group was finally looking quite good earlier this summer. After falling in a steady fashion for years, the Euro STOXX Banks Index was finally starting to show some signs of life. It broke out of a 2.5 month sideways range to the upside in early June...and made a nice “higher-low” later in that month. However, it did not follow that up with a “higher-high” in July. In fact, it got RIGHT UP to its June highs...and rolled-over. It is now testing its June lows, so there is a chance that instead of getting a nice “higher-high,” we will get a “lower-low” instead. If (repeat, IF) that happens, it will take a lot of wind out of the sails for a stronger recovery in Europe.

Having said all this, we do need to also point out that the DAX achieved a “golden cross” recently...when the rising 50 DMA crossed above a rising 200 DMA. More importantly, the ECB’s massive stimulus plan was historic...as it overturned years of opposition from northern European countries to issue common debt. In other words, there is a good chance that the recent weakness we’ve seen in certain stock markets across Europe might just be something that worked off some technical factors...and the rally will resume very soon. However, we won’t know that for a few weeks, so we’ll be watching these European markets very closely going forward.

8) As we said above, we made some comments about gold early in the week last week...and we made some comments about the dollar at the same time. Basically, we said that the DXY dollar index was becoming oversold. We also said that it could still fall a little further because the oversold readings were not quite hitting extreme levels, but that it was becoming ripe for at least a short-term bounce.

Well, it did sell-off a bit more as we moved through the week...and the readings did indeed become more extreme. For instance, its daily RSI chart for the DXY fell to 17.3 on Thursday...which is the most extreme reading it has seen since the March 2008 lows!!! So it’s no surprise that the dollar bounced pretty strongly on Friday...and it should bounce further over the very-near-term.

This does not, however, mean that the dollar has made an important low. The weekly RSI chart is not oversold. Back in 2008...when a long-term bottom in the dollar was put-in...both the daily and weekly RSI charts were quite oversold, so both of those charts were pointing to a more meaningful bottom. This time we only have the shorter-term RSI reaching extreme levels......We’d also note that even when the dollar DID make an important low back in 2008, it did not bounce-back immediately. It bounced along the bottom for many months before it finally began to rally. Therefore, we do not expect a significant bounce in the greenback...over either the short or intermediate-term.

In fact, we believe that the dollar will probably head lower over time. As we just described above, a lot of technical damage has been done to the dollar over the past two weeks. It’s “next bounce” will be important. If it fails...and the DXY rolls back over rather quickly and takes out its lows from Thursday (of 92.50)...it will confirm a change in trend for the U.S. dollar...which will have important implications on several economic (and political) fronts.

9).....On the political front, things are starting to heat up...and Vice President Biden’s pick for VP should be the starting gun for this Presidential campaign to finally move into over-drive in a substantial way. (He said he would make the pick next week...but there are now some rumblings that they might put it off until the following week.) We still think he’ll pick Kamala Harris, but there has been some opposition within the Democratic party about her. However, we could NOT BELIEVE that some Democrats are complaining that she’s too ambitious. How could anybody be so stupid as to say something like that. First of all, EVERY person who has EVER made a serious run at the top two jobs in our country has been very ambitious. (Don’t believe that “aw shucks” crap about Abe Lincoln!)....Second, when was the last time ANY man EVER was accused of being too ambitious for the VP job??? So saying that about a woman is beyond stupid.........Biden needs somebody who can attack Trump effectively. The two choices to do a great job in that capacity are Kamala Harris and Elizabeth Warren....It won’t be Elizabeth Warren.

Anyway, there was a fascinating article we read last week that questioned whether President Trump would drop out of the race before the election. No, it does NOT predict that he will drop out of the race. In fact, they say it’s highly improbable that he will. However, is still an intriguing art

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464