The Death of Petrodollars - August 5, 2015

Click Here for this Week's Full Letter

Greetings,

On a baseline level, there are two shortages squeezing financial markets at the moment. The first is a deficit of high quality collateral. The combination of fiscal austerity and quantitative easing has created an environment where demand for sovereign debt will exceed supply by $600 billion in 2015, according the JPMorgan. The second is a shortage of US Dollars (USD) flowing through the global economy. This scarcity, combined with increased demand, has created a bull market in USD that is actively tightening monetary conditions across much of the developed world.

The collateral shortfall has been covered at length since 2012, but the limited supply of USD is only now starting to become apparent. It wouldn’t be a problem if there was a shortage of Brazilian Real, for example, but USD is a different animal because it’s the world’s reserve currency. Economists call this the Triffin Dilemma, where the US must be willing to supply the world with excess currency to meet global demand, creating an implicit current account deficit.

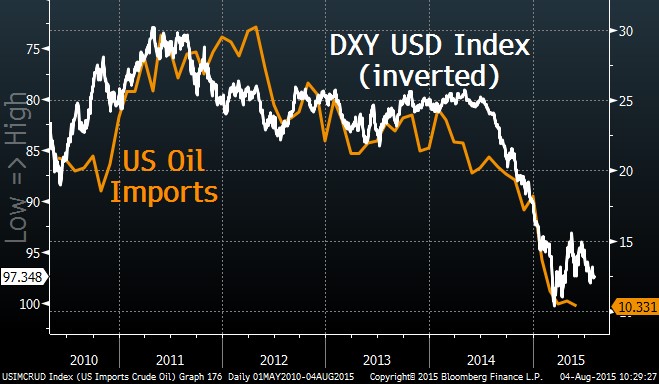

Even though the US money supply is still growing, the amount available to foreigners is shrinking rapidly due to the explosion in US oil production. Since 2011, US crude oil production has jumped 76%.

The US doesn’t export oil, meaning all of the newfound supply is consumed domestically, which puts a serious crimp in imports. In 2011, the US imported roughly $30 billion worth of oil every month, or $360 billion annually. Today, that number is closer to $120 billion annually. The $240 billion difference reflects the amount of “petrodollars” that are no longer flowing into the global economy. That might not seem like a lot of money, but it reflects what is happening across several markets.

In the early 1970’s, Richard Nixon negotiated a deal with Saudi Arabia that in exchange for arms and protection they would denominate all future oil sales in USD. Since these dollars did not circulate within the US, and thus were not part of the normal money supply, economists felt “petrodollars” was a better descriptor. Until recently, petrodollars effectively solved the Triffin Dilemma, but it looks like that era is coming to an end.

The limited supply of USD flowing internationally means that, even if demand stays flat, it will appreciate in value. However, that appreciation is guaranteed to increase demand. The stronger USD, in turn, lowers the price of oil, reducing the value of US oil imports, creating a cycle that George Soros would call reflexivity. The stronger dollar not only tightens monetary conditions in the US, but also China, which maintains a currency peg against USD. Meaning 36% of global GDP is tightening policy at a time when the global economy looks as vulnerable as it’s been since 2008.

The Cup & Handle Fund is up around 3.5% on the year, and +18.5% since August 2014 (inception). The portfolio should be doing better, but I’m struggling to combat inexplicably low volatility in equity markets. It makes little sense to me, but my views tend to be early and hopefully we’ll see the VIX above 20 soon. If you’d like to start receiving these letters click here.

Today’s letter will cover several topics, including:

- Sayonara Abe?

- Mexican Standoff

- Meanwhile, In Russia…

- Chart of the Week

With that I give you this week's letter:

August 5, 2015

As always, if you have any questions or comments or just want to vent, please send me an email at mike@cup-handle.com.

Until next time, tread lightly out there,

Michael Lingenheld

Managing Editor – Cup & Handle Macro

Recent free content from Michael Lingenheld

-

The Finale - April 21, 2016

— 4/20/16

The Finale - April 21, 2016

— 4/20/16

-

The Spring Freeze - April 6, 2016

— 4/05/16

-

Dependent on Friday's Data - March 30, 2016

— 3/29/16

-

Money For Less Than Nothing - March 23, 2016

— 3/22/16

-

Avoid the Crowds - March 16, 2016

— 3/15/16

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464