Asure Software: An Undervalued SaaS Growth Story With Substantial Upside Potential

This article is being shared to demonstrate the type of content SecretCaps' members receive.

Our most recent in-depth microcap report on Netowrk-1 Technologies is still embargoed in our Newsletter Section. Join now to access the report.

Summary

- Asure is one of our top ideas - with a growth strategy linked to three major macroeconomic trends, and new product offerings to bolster growth.

- Asure has a global footprint and a solid foundation for growth with a recent refinancing, a high level of insider ownership and recent institutional buying.

- The company’s high ~80% GM, 90% customer retention rate and 79% recurring revenue offer visibility and should result in a stronger multiple moving forward. A $116.5M NOL can cut taxes.

- With a 1.67X enterprise value/revenue and a 9.68X EV/EBITDA, Asure is extremely undervalued in comparison to its SaaS peers.

- With an 80% GM, the company can deliver $0.70 to $0.74 in EPS for 2015, with a 20x P/E ratio this equates to 150%-200% upside potential.

An extensive interview with Asure's CEO, Pat Goepel, at the conclusion of this report.

Opening:

As wage increases have been weak at around three percent for the past four years, employees are becoming dissatisfied with their situations. As employers have to maintain their workforce with less profits in a more competitive marketplace, they need a more efficient way to run their organizations. Asure's cost cutting efficiencies and cost-savings offered through its workforce and workplace management solutions are a go-to for any organization that wants to be leaner and more advanced.

Asure Software (NASDAQ:ASUR) is a cloud-based workforce management software solutions provider based in Austin, TX. Founded in 1985, Asure is a $30M microcap company with an impressive growth story. The company is profiting by saving businesses time and money. This is accomplished by streamlining workforces and workspaces into highly productive engines.

With thousands of clients and a global footprint, Asure is an established company, not a typical overvalued technology company based upon promises. Further, Asure has aligned itself with three major market trends to bolster growth - globalization, mobilization and technology.

With a conservative revenue growth rate, Asure has the potential to reach $35-$40M in revenue and an EPS of $0.70 to $0.74 in EPS for FY15. This equates to 150% to 200% upside potential with an industry average 20x P/E ratio.

A Breakdown Of Assure's Two Product Suites:

The company's AsureSpace and AsureForce each comprising various product offerings that can integrate with each other, while both product lines strive to make businesses more efficient.

AsureSpace is a scheduling and workplace management software that allows employees to book meeting space or a desk from their own mobile device, or a kiosk - improving workspace utilization. This suite includes a resource scheduler, meeting room manager, workspace manager, workplace business intelligence, smart view and integrated hardware comprising of employee's devices or touch panels and kiosks. Further, NowSpace allows you to book rooms or desks, view co-worker availability directly from your smartphone.

AsureForce comprises a suite of software, hardware and mobile workforce management solutions to improve efficiency through enhanced business intelligence to better allocate a business's workforce, decrease costs by flagging staffing issues and reduce labor expenses while creating strategy opportunities. On the software side, AsureForce Time and Labor Management Software that allows the managing of leave requests and PTO, time sheets online, employee attendance, workforce scheduling and more all from the cloud. This segment also comprises Asure's time clocks and data collection device and GeoPunch to track employees.

New Product Offerings Can Benefit Organizations - While Increasing Asure's Sales:

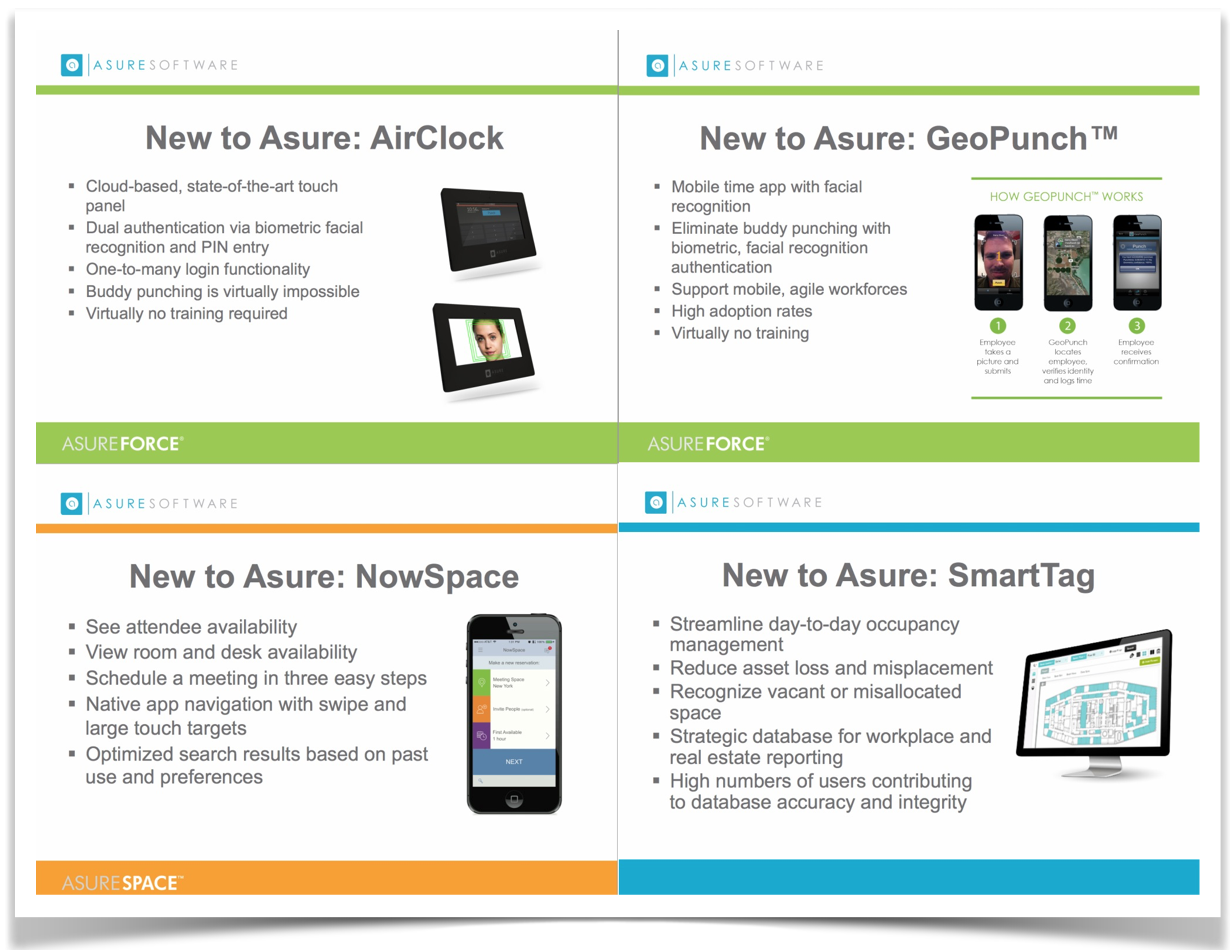

Recently, Asure has unveiled four new product offerings to complement its two key product and software suites. These new and unique products will bolster the efficiency Asure can offer to businesses while increasing sales for the company.

GeoPunch: Asure stated that their time tracking management software delivers an 80% reduction in time and attendance administration. Further, the association of Certified Fraud Examiners found that the average organization loses 5% of its annual revenue to occupational fraud. Managing new hires, an expanding business and mobile workers leads to this lost revenue. Asure's GeoPunch tracks whose working to eliminate fraud and enhance productivity. This application requires virtually no training, and eliminates the clocking in of a co-worker through facial recognition.

AirClock: The average organization pays $5720 in non-work dollars to every employee. Overall, workers spend 26% of their time at work, not working. Companies are turning from the old manual system to fully automated time clock hardware from Asure. Asure offers proximity cards, barcode cards and biometric options to eliminate time fraud and payroll costs. To the benefit of the business, Asure's options can be licensed on-demand or pay-as-you-go.

Asure's AirClock offering is a fixed cloud-based device that offers biometric facial and PIN entry for employees to check in at work. This eliminates buddy punching, and increases business efficiency as employees can be better tracked. Moreover, AirClock requires virtually no training.

NowSpace: NowSpace is Asure's easy to use solution that solves a massive problem ubiquitous to every organization - the frustration of an employee reserving a desk only to drive all the way to work to find their reserved desk is occupied due to miscommunication within the system. Asure's NowSpace is an easy to use application that allows an employee to book a room or desk to work at, when they want it. This cuts down on the real estate needed by a business and allows employees workspace only when they need it - especially as many employees are working from home, or are on the go. With NowSpace, Asure has stated that they can accommodate employee needs with up to half the physical real estate requirements. NowSpace can be used on employee devices or on employer given ones, and is an actual application - not a web based site.

SmartTag: Last on the list of new products is Asure's SmartTag. This goes beyond employees and tracks physical assets from an employee phone to a desk chair or computer monitor. This allows for reduced asset losses and misplacements and the ability to recognize vacant or misallocated space. This division is reminiscent of our article on SuperCom's (NASDAQ:SPCB) acquisition of OTI's SmartID Division. OTI's SmartID division ranged from electronic monitoring and location tracking to SmartID creation such as Passports. Although Asure's SmartTag division can only be used to track business assets. It is worth noting that SuperCom has increased roughly 300% since the acquisition, although that was based upon a highly accretive acquisition. This example demonstrate the playing field and opportunity Asure's SmartTag can target.

(click to enlarge)

A Growing Company: Refinanced With Insider Ownership And Institutional Buying:

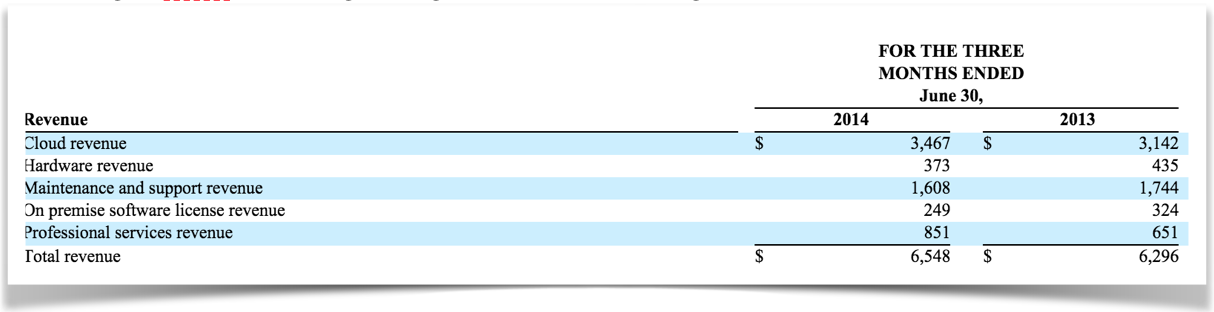

Asure's recent financials demonstrate that growth is currently underway. For the 2Q 2014, Asure reported revenue increasing 4% Y/Y, while net income increased 103% Y/Y. Asure's gross margin of 79% represented an 7% increase Y/Y. Interestingly, the company grew repetitive cloud based revenue by 10% Y/Y and saw increased cloud bookings of 83% Y/Y. Asure's net income per share improved to $0.00 per share from $(0.10) Y/Y as the company's new refinancing was in place. It is worth noting that recurring revenue amounted to 78% of total revenue in the quarter. Asure has reached a critical inflection point as the company reported a positive 2Q net income after two quarters of losses.

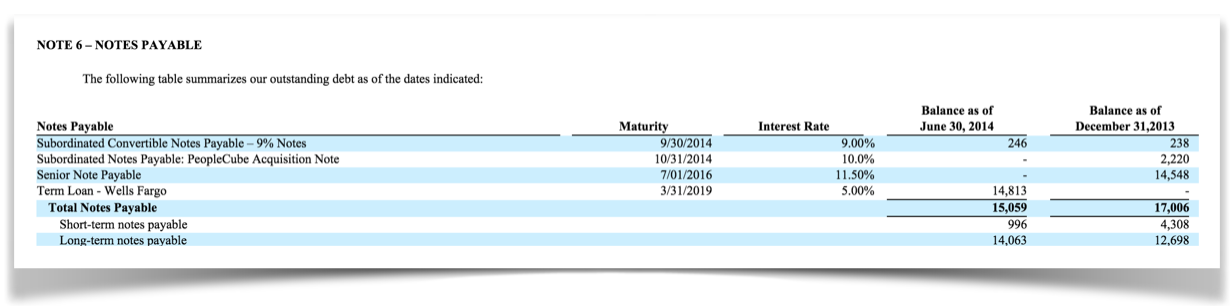

The company is becoming a leaner machine as they recently refinanced the company's senior deb under a new credit agreement with Wells Fargo. The new facility has a new term loan of $15M, a $3M revolver and an additional uncommitted incremental loan facility of $10M for future acquisitions. The new loan currently has a 5% interest rate, in comparison to the 11.5% loan agreement the company had with Deerpath Funding, LP. After incurring a one-time charge of $1.4M, Asure expects to reduce interest expenses by $0.6M in 2014, $0.7M in 2015 and reduce cash principal payments by $0.8M in 2014 and $1.1M in 2015. This will result in increased profitability for the company in 2014 and 2015.

High insider ownership of 20% demonstrates that management's goals are aligned perfectly with shareholders - eliminating any potential principal agent problem. Pat Goepel, CEO of Asure, owns 6.7% of the company and Asure's Chairman Daniel Sandberg owns 13%.

(click to enlarge)

In addition to a healthy insider ownership, institutions have begun to add to their holdings in Asure as the company grows and develops. Institutionsincreased their holdings by ~20% Q/Q. Overall, 26% of the company is owned by institutions and mutual fund owners, equating to a solid ownership level while allowing liquidity with a 4.69M share float.

A Real World Example: Scottish Water:

Many companies offer promises as to the value proposition offered by their products and services - whereas Asure has documented success to prove it. On October 14, 2014, Asure reported that they implemented an agile working program that enabled Scottish Water to save over ~$6.3M (€5M) in construction and operating costs. This was achieved in Scottish Water's new office with a 25% reduction in the number of workspaces through Asure's Workspace Manager solution to support a hot design and resource sharing system.

With almost 3,400 employees in six locations throughout Scotland, employees had faced various problems that reduced efficiency. Scottish Water's employees were spending too much time in vehicles between locations, had difficulties reserving rooms via email and lacked any form of hot desk reservation system. Together, these items caused employee frustration and reduced work efficiency.

After the implementation of the agile working program, roughly 1,500 employees use Asure's Workspace Manager to book workspaces and meeting rooms online and in the office using kiosks and touch panels. Asure's solutions also cut down significantly on the time employees spent in vehicles between locations. Asure's solutions eliminated employee frustration and allowed management to be aware of room and desk utilization. Looking ahead, a pilot program us underway which will allow employees to book carpooling, and include video conferencing resources. Per the release, Scottish Water has plans to roll out Workspace Manager hardware and software to four additional offices and is evaluating Asure's Visitor Management and Catering services.

Outside of Scottish Water, Asure closed several other deals as of last quarter. These deals include the sale of AsureForce workforce management solutions to PSSI in the U.S., and the sale of Asure Space workforce management solutions to KPMG and PriceWaterhouseCoopers in the UK. Documented success and cost savings for businesses using Asure's solutions will attract future clients for Asure moving forward.

Forward Projections and Valuations:

2014 In A Nutshell:

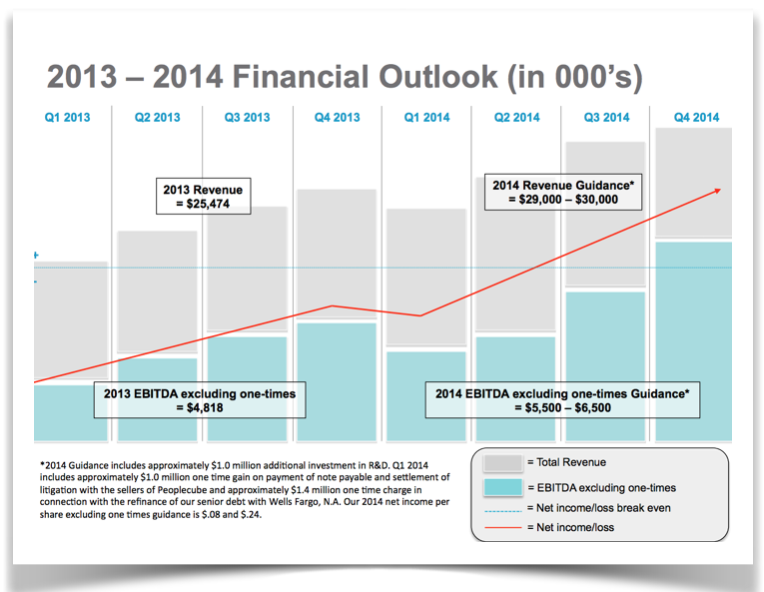

Asure's solutions are being adopted by the marketplace as they are proven to make businesses not only more efficient, but in turn more profitable. Management has provided projections for the current fiscal year that we believe are achievable based upon Asure's recent documented growth, closed deals, and the cost savings and efficiency their competitive solutions provide to businesses. Management has stated that Asure can deliver $29M-$30M in revenue and $0.08 to $0.24 in EPS for FY14'.

(click to enlarge)

2015's Projections and How This Growth Will Be Achieved:

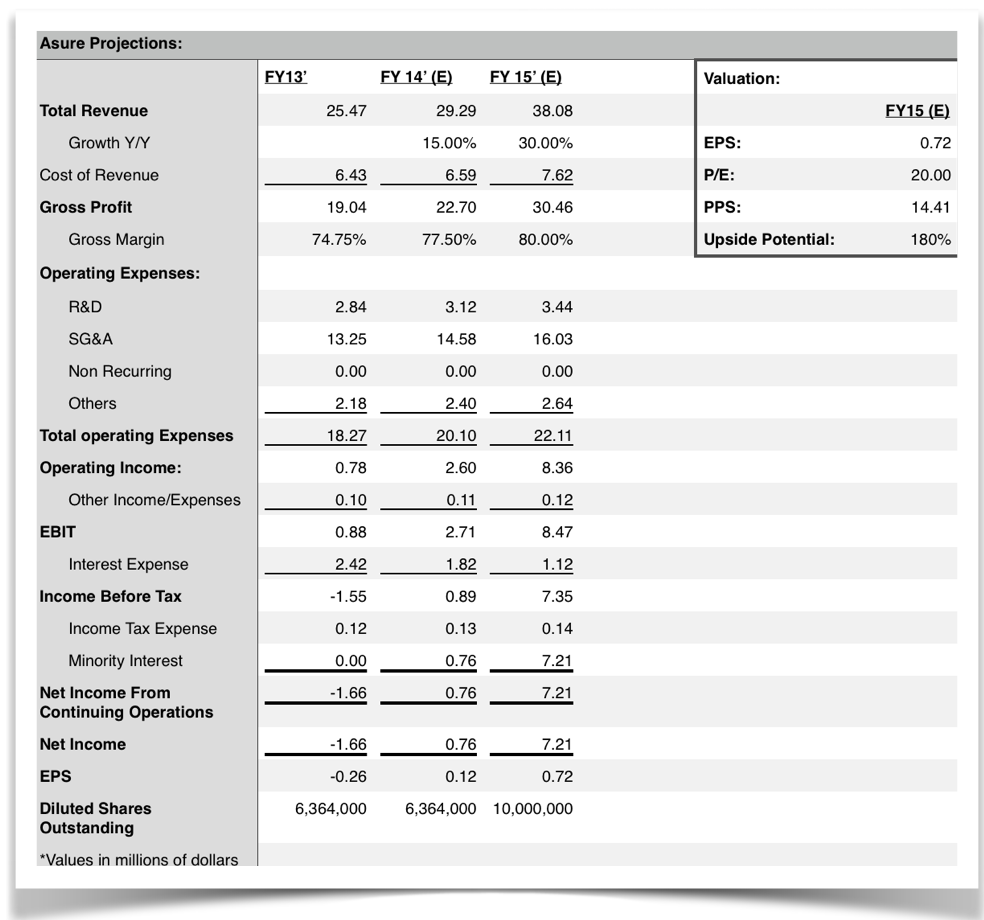

With a quarter and a half to go for FY 14', we believe looking to 2015 can provide an even more fruitful opportunity. As with other technology companies, a company's products generally have a high curved adoption curve - slow at first before high growth sets in. We believe Asure is in an excellent position to target and capture growth hinged on three macroeconomic trends that will drive top-line growth. Looking ahead to FY 15' we believe Asure can achieve revenue of $35M-$40M, and EPS of $0.70 to $0.74.

1) A High GM and Recurring Revenue Equals Visibility:

Asure's high recurring revenue ~79%, coupled with their high ~80% GM offers excellent visibility and should result in a premium multiple moving forward. This is a key reason why we believe our 20X P/E ratio used in our model is conservative. Further, as Asure continues to demonstrate growth in the coming quarters, institutions will be more willing to reward Asure with a higher multiple due to its high GM and recurring revenue level which offer excellent visibility.

With a large GM, Asure is a lean machine dropping more revenue dollars to the bottom line. Further, a high recurring revenue percentage offers a predictable growth model moving forward. Due to this visibility, the market should grant Asure a higher multiple than the industry average -the main reason why we believe our 20X P/E ratio is conservative.

2) High Client Retention And An Untapped Market:

Barrington research found that Asure has a 90% client retention rate and has only penetrated 4% of its $600M addressable market. This research estimated 150,000 potential clients paying $4,000 annually. A high client retention rate further solidifies the predictability of Asure's business model. Asure's 90% customer retention rate, coupled with its ~79% recurring revenue stream offer stable growth and high visibility moving forward. The company also has a massive untapped market that it will target in the coming quarters.

Asure's high client retention rate, gross margin and recurring revenue stream all provide for visibility and stable growth moving forward not seen in other technology or microcap companies and should provide for a stronger multiple moving forward.

3) Technology Trends:

More business are eliminating the employee backpack and increasing support for BYOD strategies - thus allowing an employee to use their own devices to achieve work results. Frost and Sullivan found that 70% of organization in the US will embrace BYOD activity, and 78% will by 2018. As such, more businesses will embrace trends which favor Asure's solutions - driving growth as Asure is a very competitive player in the field. This is noted by their new and innovative product offerings.

Further, the permeation of the cloud for businesses and employees means employees can collaborate more easily than ever before, while not having to be in the same physical location. Asure's employee tracking helps keep tabs of mobile employees, prevents clocking in a fellow employee, and allows for hot desk and meeting room bookings through their integrated apps, kiosks and smart panels. So when employees need to come into the office they can easily reserve a space - saving time, money and frustration for the employee and the business owner.

4) Mobilization Trends:

Telecommuting rose nearly 80% from 2005 -2012 and 1.3B workers will be mobile by 2015. Asure's offerings not only allow a business to better keep track of their employees through GeoPunch and other solutions, but allows the business to keep track of their physical assets that employees may utilize with SmartTag. Further, since all of Asure's offerings are integrated, Asure will be a friend to the growth in mobilization. For example, an employee can clock in on AirClock, verify their location if they run out with GeoPunch and then reserve a desk for the evening with NowSpace - all the while a business can track their physical assets with SmartTags.

5) Globalization:

With over 82,000 companies and 800,000 subsidiaries being multinational - business are more geographically stretched than ever. With multiple satellite offices ranging from a few to larger side operations with thousands of employees - businesses are craving efficiency to better track their organization and save money while doing so. Asure's offerings can virtually eliminate the26% of time workers spend at work, not working. Further, they can virtually eliminate the 5% of total revenue lost through occupational fraud. These items are more prevalent than ever as business expand geographically, with managers not being a quick walk down the hall. With Asure's offerings, the employee-manager link is re-enabled with increased efficiency.

6) Global FootPrint and Existing Clients:

With 4,161 locations in 80 countries, Asure's global footprint will ensure that it can profit from providing increased efficiencies and cost-savings to business beyond domestic borders. The work norms and operations are different in foreign countries, but the concept of business efficiency is a globally shared business goal. Asure can offer its solutions to businesses around the world, a near limitless opportunity for the small company.

With over 5,000 current clients, I believe Asure will be able to both cross-sell its new products and offer solutions these clients may not already have, to the company's benefit. If these clients purchased Asure's products in the past, the addition of Asure's newer offerings will result in increased efficiencies. Further, this proven partner channel demonstrates Asure's ability to work with and satisfy some of the world's largest companies, which can also be used as a selling point for potential new clients.

Recently, Asure partnered with Douma, Japan's only firm dedicated solely to workplace management, whihc will offer Asure's solutions to its clients. This partnershipw will help Asure bolster its revenue in a new untapped international market with the only provider in that country.

These thousands of clients include brand name companies such as Pfizer (NYSE:PFE), Staples (NASDAQ:SPLS) and Wells Fargo (NYSE:WFC). These are major companies, and signing deals with these giants should not be brushed off as an easy endeavor.

7) Targeting New Opportunities:

The market for mobile workforce programs and solutions that Asure is targeting is huge. Specifically, Steven Rodriguez, Asure's COO stated the following with regards to 2013' spending allocated to time and labor management technology.

"According to Forrester's 2013 Mobile Workforce Adoption Trends, approximately 10 percent of the $6.1 billion time and labor management technology market is spent on mobile workers. Almost two thirds of all organizations are implementing mobile workforce programs and the demand for mobile workforce solutions is growing by 23 percent."

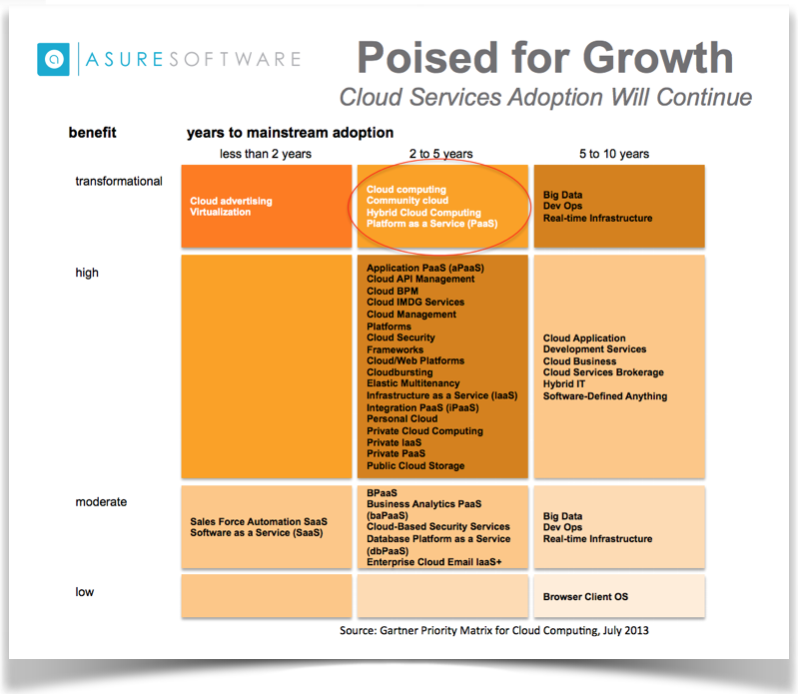

Outside of current macroeconomic spending trends, Asure is looking to expand its high-margin cloud options over the next 2-5 years. These initiatives include items such as community cloud offerings to cloud security and platform as a service or PaaS offerings. We believe that Asure aligning itself with growth initiatives in the cloud market is an excellent decision as cloud computing service revenue is projected to top $500B in 2019.

(click to enlarge)

8) Cost Savings and Efficiency Offered To Businesses Will Drive Growth

As seen with Scottish Water, Asure's offerings saved the company over $6.3M in only one location. Asure also signed deals with PSSI for AssureForce workforce management solutions in the U.S., and the sale of Asure Space workforce management solutions to KPMG and PriceWaterhouseCoopers in the UK. We believe these deals, sporting documented cost savings with large organizations, demonstrate Asure's viability in the marketplace and that the company can offer these types of savings to many organizations in the future. Since Asure is proven to save businesses money, we believe the company will not have a problem attracting future clients.

9) These Initiatives Will Lead To Impressive Growth in FY15':

Looking ahead to 2015, Asure can offer shareholders a very impressive return on a very conservative growth level for an SaaS company. To achieve the low end of management's guidance for FY14', Asure will have to grow revenue 15% this year. We believe this conservative growth rate is obtainable as the company has already reported $13.08M in revenue for the first have of 2014. Further, since the company's new product offerings have rolled out, and recent deals, such as with Scottish Water, can entice new clients to reach out to Asure for their solutions. At the low end of the revenue target of $29M, on a GM slightly below this past quarter, we believe Asure can reach $0.12 in EPS - the midpoint of management's guidance for FY14. Our low end target is in line with Kristi Richburg's, CFO of Asure, guidance for FY14.

(click to enlarge)

Turning to 2015, Asure has an opportunity to reward shareholders handsomely. Due to the cost savings and efficiencies Asure's product offerings can achieve for customers, we believe a 30% Y/Y top line growth rate is achievable as the company ramps up its offerings and unveils further cloud solutions hinged on a $500B addressable market by 2019. With a slightly expanded 80% GM as Asure has become a leaner engine, the company can deliver $0.70 to $0.74 in EPS for 2015. With a P/E ratio of 20X, this equates to 150%-200% upside potential from current levels.

We believe our model is conservative as a company's P/E ratio generally expands as the company grows, yet we have chosen the industry average P/E ratio. Further, we have accounted a notable increase to 10M S/O by 2015 to account for any increases in Asure's S/O for any future acquisitions.

We have elected to expand Asure's S/O to be conservative in out model. Although since the company is now profitable and producing a TTM operating cash flow of $2M, the company will likely not need to raise its S/O and this can result in a stronger EPS number for FY15'. Management has also stated they believe they will generate sufficient cash for its short term needs and debt requirements over the next twelve months, so there may be no reason for a raise.

We believe ~29M in revenue for 2014 is an accurate target as the company reported $7.03M in revenue alone for the quarter ending September 30, 2014. Growth is also accelerating as the company became much more profitable earning $161K for the quarter versus only $15K in the previous one.

Achieving An 80% GM For FY15':

A Leaner Machine:

Our model includes a slightly enhanced GM as Asure better handles their costs moving forward. Asure's largest operating expense, SG&A has slowed as revenue has increased, allowing for a higher gross margin. In the 2Q, SG&A increased only 1.4% Y/Y as revenue increased 4%. This is notable as SG&A accounted for 72% of Asure's operating expenses in the second quarter.

(click to enlarge)

Our model includes a 10% Y/Y increase in all expenses. A closer look reveals how Asure will be a leaner and profitable machine moving forward, even with higher expenses - specifically its SG&A load. Due to the company's refinancing of its original $14.5M in senior debt through DeerPath with Wells Fargo. This resulted in Asure's interest expense decreases $0.6M in 2014 and $0.7M in 2015. Without this decrease, keeping interest expense even Y/Y, Asure would only deliver $0.03 in EPS in 2014, ceteris parbius. This refinancing will also reduce principal payments by $1.9M over the next two years as well.

In addition, in March 2012, Asure amended the terms of the $1.5M convertible notes bearing 9% interest the company issues to finance its acquisition of ADI. Under the amendment, each 9% notes holder was permitted to convert the balance into common stock at $5 per share. $1.15M of the $1.5M was converted - eliminating a large portion of this 9% debt burden.

Further, In July 2012, Asure issued a $3M note to the seller in its acquisition of PeopleCube. Asure had a dispute with the PeopleCube and Meeting Maker over a post-closing adjustment. The parties agreed in February 2014 to reduce the original $3M amount by $540K. The parties then settled and dismissed all litigation after settling the then $2.46M note for $1.7M. Asure's insurance carrier also agreed to pay Asure $500K in conjunction with the settlement. The end resulting in Asure recording a net gain of $1.034M recognized in the 1Q of 2014. This note had an outstanding balance last fiscal year of $2.22M at 10% interest - and this has now been eliminated as well.

Overall, Asure has become a much leaner and cost efficient machine as the company's outstanding debt at the various interest rates of 9%, 10% and 11.50% have mostly been paid off or refinanced to 5%. This allows Asure to drop more money to the bottom line, also known as a higher GM.

Growth In Higher Margin Cloud Offerings:

Asure's cloud revenue inherently has higher margins than its hardware segment. As Asure continues to grow its cloud offerings, and offer more as demonstrated in their 2-3 year growth scenario, the company's GM should stabilize at 80%, from 74.75% in 2013. We believe this is obtainable as last quarter's 79% GM increased 7% Y/Y. In addition to higher margin cloud revenue, Asure has two other items bolstering its GM.

(click to enlarge)

Coupled with Asure's excellent moves to refinance their debt to entail much lower interest expenses, the slowing growth of the company's highest op-ex metric SG&A and an emphasis on highe

Recent free content from SecretCaps PRO

-

SecretCaps: Operational Update

— 10/31/16

SecretCaps: Operational Update

— 10/31/16

-

Total Telcom: A Virtually Unknown NanoCap With A Spark

— 9/28/16

-

Spindle’s Experienced Management Overhaul Has Caught Our Attention

— 8/31/16

-

MicroCaps: Seriously, The Last Frontier

— 6/30/16

-

MicroCap Digest: Atman's Acquisition and BeWhere's Insider Buys

— 6/10/16

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464