THE WEEKLY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) Russia/Ukraine…the Fed…Leverage. The unwinding of leverage is the most important threat.

2) Earnings estimates are about to fall out of bed.

3) Peabody Energy’s issue last week was much more than just a “mismatch margin call.”

4) Banks (who are also “hedge providers”) seem to be vulnerable right here.

5) Updates on the charts for the S&P 500 and NDX Nasdaq 100.

6) Many chip stocks (and their ETF) are very close to key support levels.

7) AAPL has broken a couple of support levels…as is now close to a third (more important) one.

8) Russian bonds are not the only ones that have seen significant weakness recently.

9) Do you want to buy China on weakness? Forget BABA, look at the FXI.

10) Summary of our current stance.

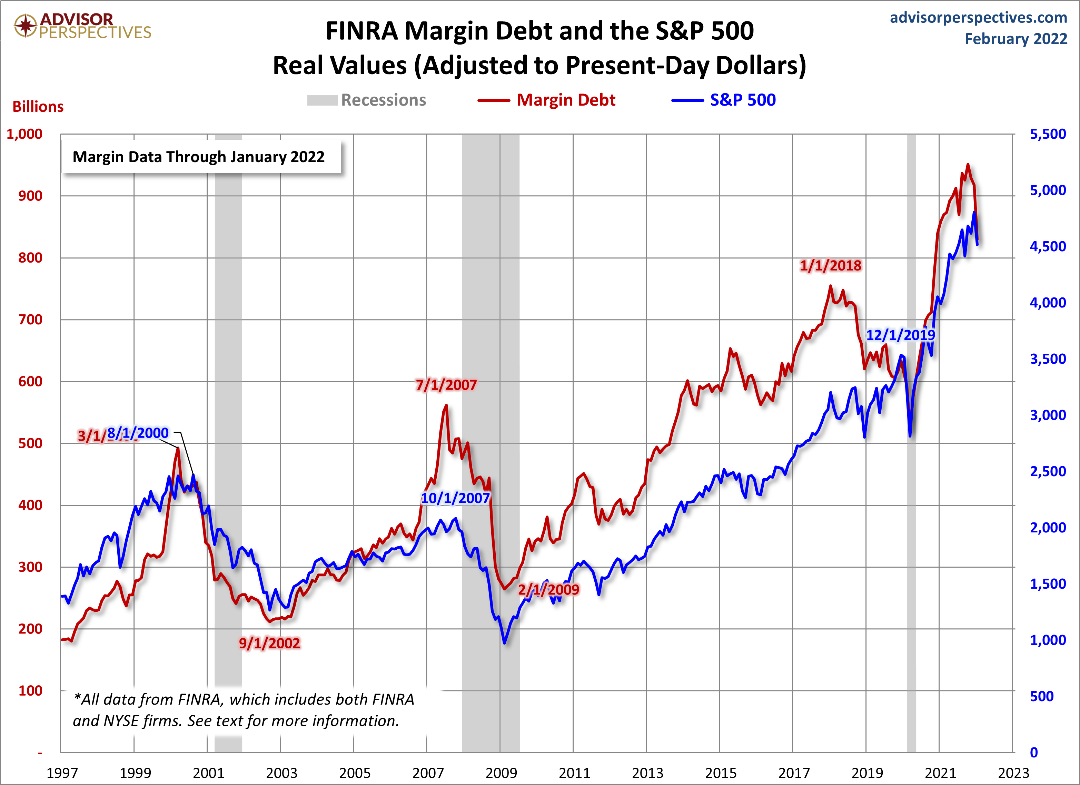

1) Investors are focusing on every little development that comes out of eastern Europe…and for good reason. They are also paying very close attention to the Fed (which will be especially true this week…with the announcement/press conference on Wednesday). However, the most important issue facing the markets right now is the massive levels of leverage that still exist in the system. One way or the other, it is going to be unwound further…in a meaningful way. The only question now is how fast it will be unwound.

The stock market (and most other markets) spent most of last week bouncing around in reaction to any new-news out of eastern Europe. This makes total sense. If this situation can suddenly calm down in a significant way, it’s going to give the stock market a VERY strong short-term rally. It will also have a very big short-term impact on many different groups (i.e. bullish for travel/leisure…bearish for energy). If, however, the crisis drags out over an extended period of time, it’s going to heighten the issue of inflation even higher…and also raise the specter of stagflation as well.

(Actually, we don’t think it makes “total sense.” The odds that Putin is going to do what it takes to calm this crisis any time soon…based on what we hear/read from the geopolitical experts we respect…are VERY low. Therefore, we think the stock market should move considerably low immediately. However, we’ve been doing this long enough to know that the stock market ONLY does what it SHOULD do…eventually. Thus, we do expect many more sharp moves in both directions over the near-term.)

The other big issue at the forefront of everybody’s mind is the one that was already creating significant headwinds for the stock market before the Russian invasion of Ukraine. Needless to say, we’re talking about monetary policy. The Fed’s decision to dramatically change their monetary policy…from one of momentous (and historic) levels of stimulus and liquidity…to one of tightening-back on that record levels of accommodation (without stopping at neutral) has made it A LOT HARDER to justify the extreme valuation levels that existed at the beginning of the year. Even though Chairman Powell has said that they’re not going to be as aggressive as some of their members had been saying before the invasion of Ukraine took place, they are still going to be a lot more aggressive than they were saying (or the stock market was pricing-in) during the autumn months of last year.

However, the most important issue facing the markets right now…and it is being (and will continue to be) effected by the two above-mentioned issues…is issue of leverage. The second issue we highlighted (the Fed) played an important role in the enormous accumulation of leverage over the past two years (and more). The Fed’s massive liquidity program gave investors the kind of confidence to take A LOT more risk…and add A LOT more leverage to their portfolios. However, now that they have made a 180 degree turn in their monetary policy, it means that these leveraged investors and traders will have no choice but to (continue to) unwind a substantial amount of the leverage they have acquired in recent years.

There is little question that the Fed will start raising rates next week. This will be the second step in their tightening policy…with the “tapering” of their QE program being the first step. (“Tapering” IS tightening…no matter what anybody else says. When you go from massive levels of steroids…and then start using lower levels…you get weaker.) Therefore, as the Fed continues on tighten even more, leveraged investors will have to unwind more of their leverage.

This takes us back to the first issue we raised…the crisis in eastern Europe. Even if this crisis did not appear on the landscape, investors were going to HAVE to unwind a lot of leverage one way or the other (due to the Fed’s big change in policy). However, with invasion of Ukraine…and the acceleration of inflation it has caused…investors have had to unwind some of their leverage even faster than they would have if Mr. Putin never invaded his neighbor.

SO now the question is merely, how fast will these leveraged investors have to unwind??? If the crisis in eastern Europe continues (as we expect it to), the unwinding of all that leverage will come quite quickly. If the crisis calms down in a material way, the unwinding process will take longer to playout. However, it will STILL take place…because the Fed will still be tightening. In fact, they’ll be able to do so in a more aggressive fashion.

Most people thing they are a lot smarter than the really are. (Even the ones with sky high IQs think they’re smarter than they really are.) This is very true in the markets…ESPECAILLY when the influx of stimulus adds high levels of leverage to the marketplace. Few people realize how much the issues of stimulus and leverage play a role when the market is flying higher. They assume it’s just their own “smarts”…and nothing else. However, when the stimulus fades…and the leverage needs to be unwound…the truth becomes apparent…even to extremely smart people. (Just ask Cathie Wood.)

Source: FINRA via Advisor Perspective

2) It is incomprehensible to us that the consensus earnings estimates have not come down in a serious manner. Analysts are likely waiting for Q1 earnings to be released, but with the significant change in the economic outlook…and the inflation picture…it is only a matter of time before the 2022 earnings estimates are lowered significantly. Therefore, as the “E” part of the forward P/E ratio comes down, the 18.7x forward number we’re seeing right now will have to go up. In other words, the stock market is not getting cheaper to the degree that some people think after this recent decline in the major averages.

Long before Russia invaded Ukraine, the earnings picture in the U.S. had been deteriorating for months. We probably shouldn’t use the word “deteriorating”…because the picture was merely becoming “not as good.” It was not getting “worse.” However, there is no question that during the time when the earnings for Q1 and Q2 were being reported last year, the forward estimates rose substantial (by more than 20% over the two combined quarter). However, during the time the Q3 and Q4 earnings were being reported, earnings estimates barely rose at all. They remained in the $223-$225 range on the S&P 500 for 2022.

This is where the estimates still stand today. We’re guessing that one of the key reasons why they did not rise in the last months of 2021 and in the early part of this year because analysts had become worried about the impact of the Fed’s change in policy (to a much more aggressive tightening move) would have on the economy…and thus earnings. (It would probably be more accurate to say that the companies themselves were likely telling analysts that the Fed’s change in policy to a much more aggressive tightening cycle would create headwinds for their earnings growth.)

Okay, let’s repeat the first sentence from the previous paragraph. “This is where the estimates still stand today.” Think about that. Despite the big change in the Fed’s strategy to a more hawkish/aggressive for their tightening policy (which was confirmed in December)…and despite the development of a major crisis in eastern Europe (which has taken the already extremely high inflation expectations through the roof)…the consensus earnings estimates for 2022 are still pretty much the same as they were before Thanksgiving of last year!!!.....This has to be one of the all time instances for when the term “WTF” should be used!

Just look at the estimates for GDP growth. Goldman Sachs cut their GDP growth number once again last week…and is now looking for growth of just 1.75%. In early October, they were looking for GDP growth of 4.4%!!!! How in the world can we have a situation where a MAJOR investment bank cuts their GDP forecast from 4.4% to just 1.75% for a given year...and the consensus earnings estimates stay the same???? The situation gets even more ridiculous. The Atlanta Fed’s GDPNow estimate has fallen to just 0.5%. Are we really going to get close to 10% growth in earnings…with just 0.5% GDP growth???

Needless to say, the higher input costs that the skyrocketing price of energy and materials are creating is very likely going to have a negative impact on margins. It’s great that many pundits are confident that they’ll be able to pass on these increased costs to consumers…but at some point “demand destruction” WILL take place. People who have filled up their gas tank or gone to the grocery store know that inflation is really even worse than last week’s CPI number told us……Besides, people HAVE to eat. The growing season in much of Ukraine will not take place this year…and around the rest of the world, the fertilizer prices are now set in stone. (Farmers will be planting very soon in the northern hemisphere. If there is any drop in fertilizer prices soon…which seems very unlikely anyway…will come too late. Food prices are going to be sky high this year…even if the crisis in Ukraine eases immediately.)

We haven’t even touched on the renewed disruptions in the global supply chains…or the increased odds that many countries will now pull production of many different products back into their own countries (due to these renewed supply chain problems). This will reverse the multi-decade globalization process that kept costs very low in so many different industries.

On top of Goldman’s (and others) lowering of GDP estimates, we’ve also heard many pundits say that the odds of a recession are rising. (Some of them are pointing to the move in the markets…and use those moves to determine their estimate for the odds of a recession.) Goldman has put the odds at 35%...and we have heard some people say that the odd of a recession are not as high as 50%. We think those odds are WAY too low.

We are market strategists, not economists…but we believe that the odds that a recession starts this year are over 90%. Yes, you can sit back and analyze the data on ISM, retail sales, consumer confidence, GDP, employment, CPI, etc. etc……OR, you can simply drive to the supermarket and then stop at the gas station on your way home. (Or if you want to stay home, you can just look at the yield curve.) Either way, it’s as plain as the nose on your face…we’re headed for a recession.

This means that earnings estimates are going to come down…and therefore the forward P/E ratio on the S&P 500 has not dropped as much as the bulls think it has this year. The market is still very expensive…and thus it will fall further before a long-term bottom is put in place.

3) Early last week, we all learned that Peabody Energy (BTU) had a major margin call…and shortly after that, we heard about the massive losses by a major China hedge fund in the nickel market. We’re told that BTU’s issue was just a mismatch margin call, but that is not an accurate description. As for the Chinese hedge fund, JPM is the biggest counterparty for their big short bets. If this is more than a one-off situation (like Archegos was), it won’t be a big problem. However, given the HUGE swings we’ve seen in recent weeks in the markets…and likely (big) losses they’ve likely created…this could/should become a bigger problem than most people realize right now.

At the beginning of last week, we all heard that BTU had received a sizeable margin call over the weekend…and they needed to get a $150mm line of credit from Goldman Sachs. This was not seen as a big deal…with some people calling it merely a “mismatch margin call.” However, that is misleading description. What if the end buyer of the coal had decided not to take delivery? That is not out of the question when a massive price increase takes place. Sure, they would have a contract, but what if the end-user decided to renege on the contract…and just said that they just weren’t going to pay the big price increase? If the end user doesn’t take the shipment, and thus BTU doesn’t make the sale…they don’t have the money payoff the hedge provider! If that happens, the whole thing unravels. In fact, it’s a good bet that this is exactly what took place with the big blow up in the nickel market last week.

Needless to say, that could cause some big problems for those who sell hedges to these hedge funds. This will not a big problem…if the big losses are isolated to just entity…like it was with Archegos a year ago. However, if the losses are more widespread…with many different hedge funds suffering significant losses on their highly leveraged bets…it can easily become a MUCH BIGGER problem!. Again, given the HUGE moves we’ve seen in several different markets this year…and even some individual stocks during the recent earnings season…the odds are quite high that some other hedge funds have indeed seen some very painful losses.

Midday on Friday, it was reported that JP Morgan (JPM) is the biggest counterparty risk for China’s hedge fund that made those short bets. The stock was unchanged on the day when that news hit the tape, but it fell more than2% almost immediately. Now, a 2% drop is not the end of the world, but it does show that this is the kind of news that could become a problem going forward…if other firms run into similar problems……Don’t get us wrong, we are NOT saying ANYTHING negative about JPM’s financial condition. We’re just saying that if this becomes a much bigger issue…reach is a REAL possibility…it could cause some strains for at least some financial institutions.

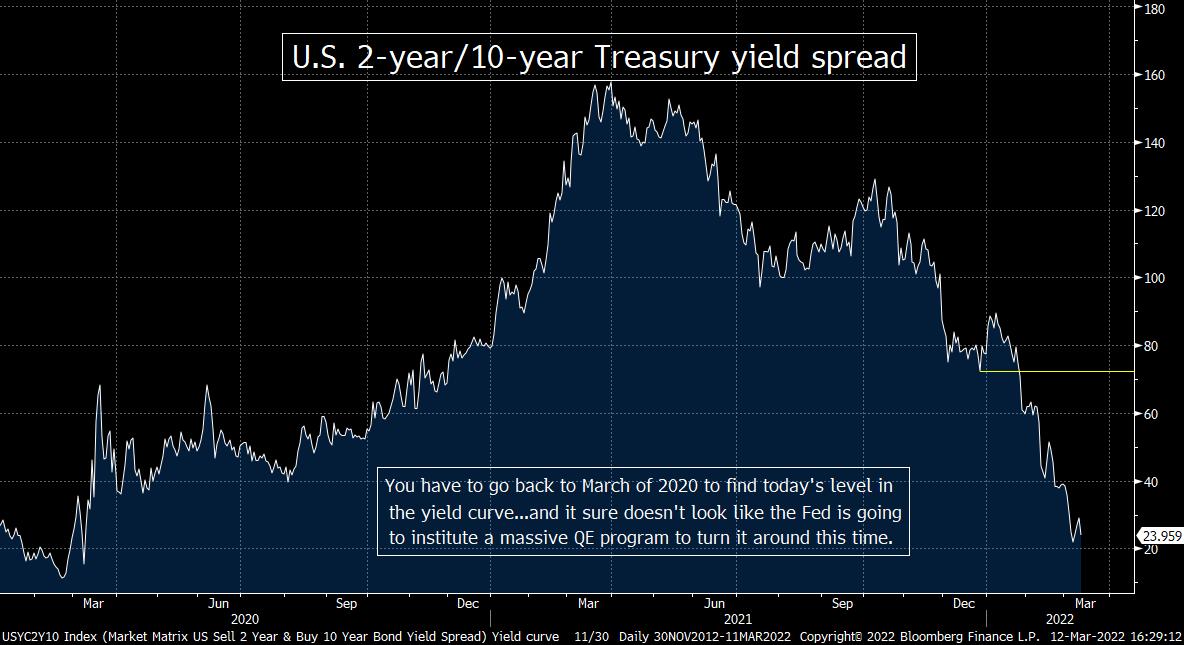

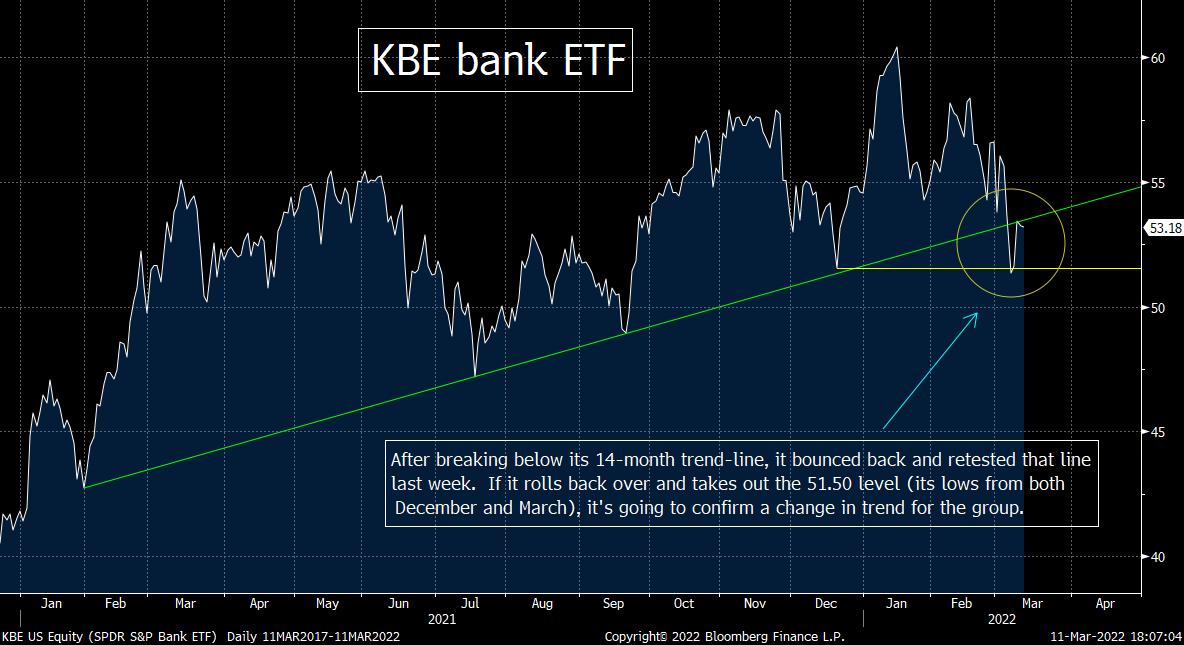

4) The “hedge providers” we mentioned in the previous bullet point includes a lot of banks. Therefore, they could (and probably will) continue to see some weakness going forward…especially since the yield curve continues to flatten. We’ll be watching the $51.50 level in the KBE bank ETF going forward. If it breaks below that level in any meaningful way, it’s going to raise a big red flag on this group.

We saw a decent sized rise in the U.S. 10-year yield last week…as it rose from 1.72% to slightly above 2% by Friday’s close. However, this was not enough to help the bank stocks…as the KBE bank ETF finished the week in negative territory. One of the reasons for this poor performance is due to the fact that although long-term rates rose, so did short-term rates. Therefore, the yield curve actually flattened last week…with the 2yr/10yr spread falling just below 24 basis point. (It’s funny how some pundits say other spreads are more important…but it’s also funny how they never say that until 2yr/10yr spread gets dangerously flat.) Anyway, since the bank margins are quite dependent on the spread between short and long-term rates, it’s no surprise that they had a rough week in the face a spike in the yield on the 10yr note.

Needless to say, the news that we highlighted in the previous bullet point about JPM’s exposure to the hedge fund giant in China who got squeezed so badly in the nickel market did not help the group late last week either. We have heard about very large losses in several other spots around the Street…like BlackRock, Aravt Global, Autonomy Capital, and others. The concerning thing is that these big loses did not start with the huge moves in the currency markets. Many hedge funds had big loses during the drop in the stock market in January…and the massive moves in many individual stocks continued well into February, so it was no picnic last month either.

Let’s face it, you don’t see double-digit percent moves in a lot of large cap names during earnings season. Sure, they can rise or fall 4%-6% or so…and we frequently see double digit moves in some small cap stocks in reaction to their earnings. However, the only way you see the monster moves that took place this earnings season in many different mid and large-cap names is because leveraged players got caught on the wrong side the market…and were burned quite badly. This means nickel and coal traders were the only ones who heard the words, “margin call Duke boys” this year.

With this in mind, we’ll be keeping our ear to the ground to hear about any other blowups around the street. We’ll also be looking for any unusual moves in any of the important financial stocks. Right now, our focus will be on the KBE ETF and JPM’s stock…and we’d like end this bullet point by reviewing the charts of both.

For the KBE bank ETF, it has recently fallen below its 8-month trend-line from last summer. It has bounced off the $51.50 level in each of the last two months. Therefore, it will be important that it holds that level going forward. If it breaks below it in any meaningful way, its first “lower-high/lower-low” sequence since the pandemic lows. Thus, if the break below the multi-month trend line is followed by a “lower-low,” it’s going to indicate that the group has begun another leg lower in the correction that began in January. (First chart below.)

As for JPM, it is getting somewhat oversold. No, the reading is not an extreme one, so it could certainly fall further…but our call two weeks ago about the vulnerability of this stock turned out to be quite prescient. It fell below $140…and that was indeed followed by a further decline. The next support level comes-in at the $125 level (which is the 50% retracement of the rally from the March 2020 pandemic lows.

JPM is a great bank with great management. However, that doesn’t mean they cannot make mistakes…or that their stock cannot see an outsized drop every once in a while. Let’s face it, JPM’s stock is now trading at the same level it stood in November of 2019!.....There should be a fabulous buying opportunity for JPM in the coming weeks, but if they have some more “counterparty” issues, that opportunity could come at a lower level.

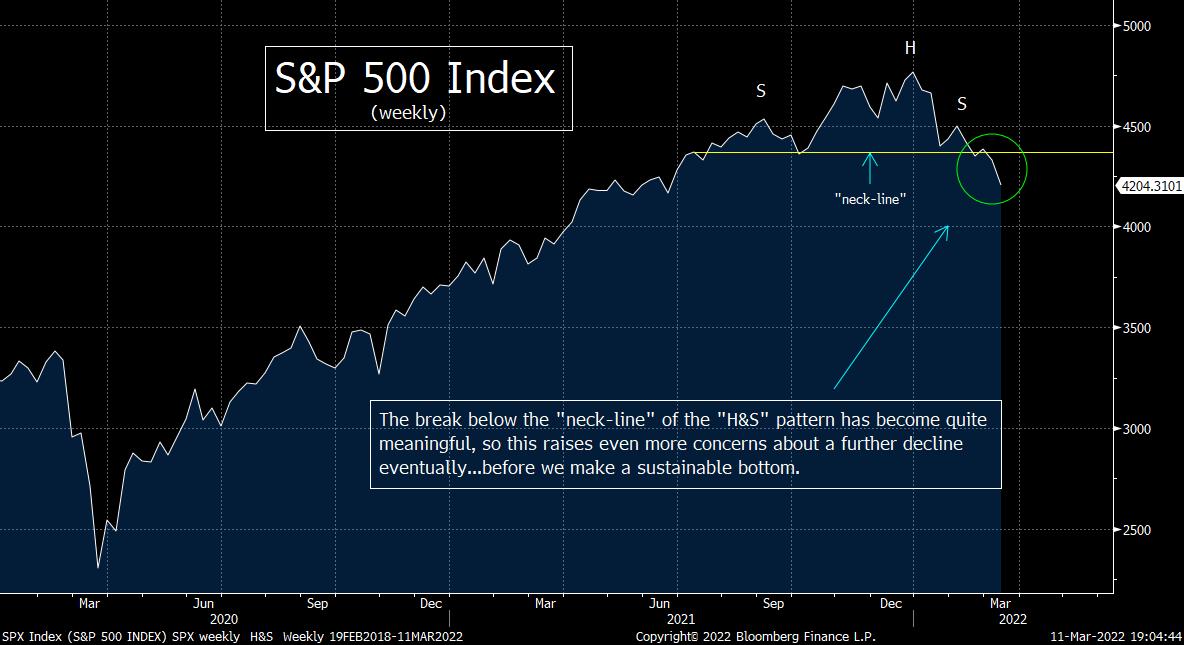

5) Last week gave us another one where the stock market moved more than 1% on every single day…and the average move on the S&P 500 was 2.2%. The average move for the NDX Nasdaq 100 Index was over 3%...with two days over 4%...so it was another volatile week. That said, the technical picture did not change all that much for these two indices. Yes, they are now both below the “neck-lines” of the “H&S” patterns, but neither has broken their more important support levels. Even tough the most important levels have not changed, we still thought it was important to highlight them again this weekend…in case any of them are broken (in either direction) next week.

It was another wild week in the stock market last week…as the SP&P 500 Index and the NDX Nasdq 100 Index both saw ranges of over 1% each day. In fact, the average daily move was more than 2% for the SPX…and more than 3% for the NDX. They both finished the week in the red…with the S&P falling 2.88% and the NDX giving back 3.87%. This took the S&P further below the “neck-line” of its “head & shoulders” pattern…and the Nasdaq did finally fall below the neck-line of its own H&S pattern last week as well.

However, neither one broke below their more important support levels (and they obviously didn’t break above their resistance levels). Therefore, these levels have not changed this weekend. However, given the unusually high volatility were seeing right now, these levels are still very important, so we wanted to reiterate them again this weekend. Besides, with so much going on in eastern Europe…and the Fed announcement/press conference this coming Wednesday…one or more of these levels could easily be broken soon. If they are, it will be a very compelling event on the technical side of things, so we thought it was important to repeat them.

Before we do that, we’d just highlight that the “death cross” in the NDX became more prominent last week (and the 200-DMA is now falling, so it’s official). We’re getting very close to the same “cross” in the S&P, so it’s something to be watching for next week…..We do want to reiterate that these kinds of negative crosses do tend to be compelling indicator for further weakness. No, they were not followed by larger declines in 2020, but that’s only because the Fed came in with the massive QE program…just after the “crosses” took place. Therefore, the technical situation is not good one right now. (Duh.)

We’re looking at the weekly chart on the S&P 500 again this week. In that chart, we can see that the 50-week moving average has stopped the rallies dead in its tracks a couple of times recently. Therefore, the new “first resistance” level will be that 50-week MA…which stands at 4,411. This is not a major resistance level, but it would certainly give the stock market some relief if we broke above that moving average…..The next (more important resistance) comes in at the level we highlighted last weekend…the 4590 level (the highs from early February).

As for support, as we just mentioned, the first support (the neck-line of its “H&S” pattern) was indeed broken. Therefore, we are now using the lows from two weeks ago of 4,114 as the next key support level. Any meaningful break below 4,100 would confirm the breakdown from the “H&S” pattern…which, in turn, would confirm that a new leg of the 2022 decline is likely to be an ugly one.

Turning to the NDX Nasdaq 100 index, the key support levels remain the same. (Remember, we’re using the NDX 100 instead of the Nasdaq Composite Index because the QQQ Nasdaq ETF corresponds to the NDX, and the most popular stocks in the Nasdaq are in that key index.) The key resistance level for the NDX is the February highs of 15,140. Any significant break above that level would give it a nice “higher-high”…and THAT would ease a lot of tensions in the marketplace.

As for the support levels on the NDX Nasdaq 100 Index, it did break below the “neck-line” of its own “H&S” pattern, so this raises our concerns even more than we had last week…because it also gave the tech laden index a key “lower-low.” This in turn made the “death cross” on the NDX a more pronounced one (and since the 200-DMA is now declining the negative “cross” is official.)…..Therefore, the level we are now watching closely it the late February intraday lows of 13,000 (13,065 to be exact). That is also very close to a Fibonacci 38.2% retracement of the entire rally from the pandemic lows to the highs from the beginning of this January…as well as the lows from March of last year (2021). Therefore, any significant break below 13,000 on the NDX would certainly be quite bearish on a technical basis

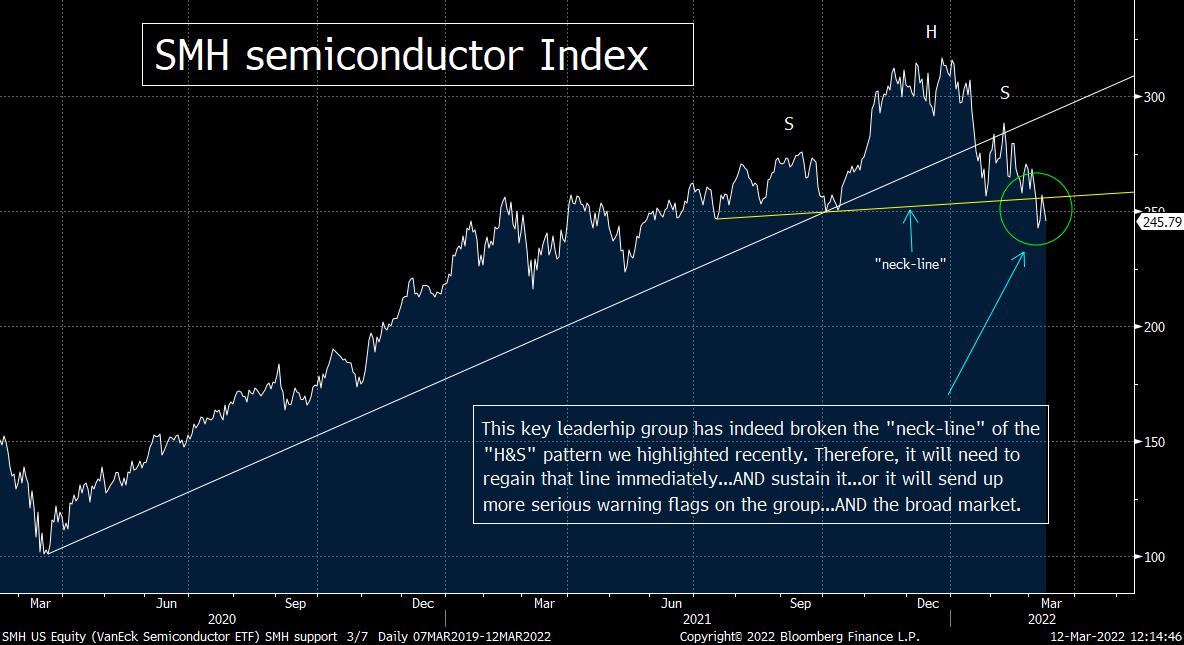

6) There is no question that the semiconductor stocks have been acting very poorly this year. We have highlighted the group’s “head & shoulders” pattern several times this year…and it has broken below that pattern quite recently……The chip stocks have been an incredibly important leadership groups for more than two decades, so this underperformance is not a good development at all. We’d also note that the charts on several key individual stocks do not look good either. With this in mind, we like to update the charts on the SMH semiconductor ETF…as well as the charts on several of the key stocks in this industry. (NVDA, AMD, MU)

The chip stocks have had a very rough year this year…as the SMH semiconductor has fallen more than 22% from its late December highs. More importantly, on the technical side of things, it has also broken below the “neck-line” of the “head & shoulders” pattern that we have been harping on in recent weeks. The SMH tried to rally back and regain that key support line midweek last week, but it rolled back over by Friday. This is quite disappointing…because the chip ETF had already broken below its trend-line going back to the March 2020 pandemic lows in January. It did bounce back and retest that line…but then it rolled back over in a meaningful way. If the recent “retest” of the “neck-line” fails as badly as the retest of the trend-line did last month, it’s going to be a very bearish development for this key leadership group. (First chart below.)

As for some specific names, we want to focus on the charts of NVDA, AMD and MU. NVDA and AMD have both formed “descending triangle” patterns…and both are close to testing the bottom lines of those patterns. For NVDA, that key support line comes in at about the $210 level…and for AMD, it comes in at $100. Any meaningful break below these levels for these stocks will be quite bearish on a technical basis for them.

These are GREAT companies…with GREAT prospects…but even the stocks of great companies can (and do) get hit hard every once in a while. In fact, these kinds of moves (where the baby is thrown out with the bathwater) creates fabulous buying opportunities. However, the opportunities just might come at levels that are materially below their current levels…if they break their key support levels soon. (2nd and 3rdcharts below.)

Finally, MU failed once again to take out its key resistance level in February (its “double top” high from April of 2021 and January of this year). In fact, it made a slight “lower-high.” This has been followed by a “lower-low” (below the late January low)…so this is a disappointing development. Therefore, it’s going to have to bounce back VERY soon, or it will likely have to retest its October lows near $65 before it can stabilize. MU is getting oversold on its RSI chart, but not extremely so…thus a further decline is not out of the question.

So as you can see, the chip stocks need to bounce back very, very soon…or it’s going to keep the level of bearishness in the market quite high. (Remember, bearish sentiment can stay very elevated for long periods of time every once in a while.)

7) In the big cap tech space, the situation in not good either. GOOGL saw a “death cross” last week, but we’re even more concerned about the action in AAPL. It broke below two support levels last week…and is now close to testing another. This stock had been seen as a “safety” stock earlier in the quarter. However, now we worry that it could become a “source of cash” if margin calls or other “forced selling” hits the marketplace.

In the large-cap tech area, GOOGL saw its 50-DMA cross below its 200-DMA last week, so that is a concern. However, our biggest concerns in this part of the stock market surrounds the action in AAPL. The stock had been seen as a very “safe” on at the beginning of this decline in the stock market back in January…and held up better than most stocks. However, it has started to decline in a more material way more recently. It has broken a couple of key support levels…and is close to testing another.

This more recent underperformance is not a big surprise to us…for two reasons. As we have highlighted in the past, when the small and mid-sized names underperform the big cap names, those bigger stocks tend to eventually decline in a meaningful way as well. (The small & mid-cap names rarely bounce back to meet the elevated large-cap names. So, the fact that 40% of the Nasdaq has already fallen 50% is not a reason to be bullish. It’s not a reason to think that the market has already seen its bear market…and thus there is nothing to worry about.)

Second, when the broad stock market (and even other asset classes) see significant declines, the biggest names frequently become “sources of cash” if/when leveraged investors get margin calls. Even though a stock like AAPL can be seen as a “safe” holding, this is the exact thing that helps it become a liquid asset that leveraged investors can actually sell when they’re trying to meet those margin calls. (Sometimes those “other assets” are not liquid enough to raise the kind of money needed to meet these margin calls.)

This is exactly what Long Term Capital Management did in the late 1990s. Their bond positions were VERY illiquid, so they had to sell massive amounts of GE stock (which was one of the biggest, most liquid stocks in the market back then.)……..In other words, it’s not just margin calls in the stock market that can lead to sales of certain big cap names. Sometimes, those stocks are sold by holders of other assets…because they’re the only ones that have the liquidity to raise the money they need……Given the massive moves we’ve seen in many different markets

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464