THE WEEKLY TOP 10

THE WEEKY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) The impact of “gamma” and “dynamic hedging” could indeed create a “melt-up” into year-end.

2) Great earnings season, but they are a long way from catching up to the level of the stock market.

3) When the world’s 2nd largest economy shifts gears significantly, it HAS to have an impact eventually.

4) Some fabulous highflying tech stocks are very overbought right now.

5) A rise above the 2021 highs on the 10yr yield is a higher possibility than most people think.

6) Strong breakout in gold last week!

7) Despite the strong dollar, emerging markets look good on the charts.

8) Somebody is betting that a big pickup in volatility in corporate bonds is just around the corner.

9) Boeing (BA) could (repeat, COULD) actually see a nice upside move going forward.

10) Summary of our current stance….Divergence between consumer spending & consumer confidence.

1) There has been a lot made of the potential for a “melt-up” in the stock market between now and the end of the year. We are not looking for such a move, but we do believe that it is certainly possible. In the options market, we could continue to see the impact of “gamma”… to squeeze the market higher. Also, in the OTC options market, it is possible that “dynamic hedging” (which is has the same impact as “gamma”) could push the market higher as well.

A lot has been made about the time impact of “gamma” recently…in terms of the individual stocks (both meme stocks and some of the other highflyers). Basically, when an investor buys a call options, the broker/dealer goes out and hedges their position. The dealer sells these options short (an “opening” trade) and they hedge the position by going out and purchasing the stock or ETF. If a large number of options players buy a large number of call options all at the same/similar time, it causes a “squeeze” on the stock……The broker dealers have no choice but to go out and buy the stock…without any thought about the stocks valuation/fundamentals. It’s “forced buying.” (If there is a large short position in the stock, the move feeds on itself…gets exacerbated even more.)

We have seen this in many meme stocks this year…with the most egregious one in recent weeks being Avis (CAR). When it affects meme stocks, it pushes the individual names higher in a massive way. However, when it pushes larger names higher…ones that have large weighting in index ETFs…it has an impact on the entire market. The most recent examples of this have been TSLA (with its 1-month rally of over 50% to the November 4th high) and NVDA (with a similar 50%+ 1-month rally…after it had already rallied 75% YTD before the October rally)! When you combine this with the 20% rally in MFST, you had 20% of the NDX Nasdaq 100 rallying in a parabolic fashion…and this helped push the entire stock market higher. (That’s right, those three stocks make up more than 20% of the NDX.)

Therefore, if these stocks…or a small number of other highly weighted stocks (like AAPL, AMZN, FB…which have been lagging recently)…start to rally in a strong way, the impact of “gamma” could help the market “melt-up” into year-end.

However, there is also another way. When the stock market rallies in a big way in any given year, some institutional investors start to get nervous. This is especially true when the market become expensive (like it is now). Therefore, some of them decide that they want some protection…in case the market rolls-over in a big way at the end of the year. This could ruin their performance (and their bonuses). Therefore, sometimes they go out and buy some put options on the S&P 500.

However, these institutions have very large portfolios…which would be very expensive to hedge. So these institutions only hedge themselves against a BIG decline. (They’re not worried about a 3-5% drop…they’re worried about a 20% drop.) Therefore, they buy put options that are well out-of-the-money…which are MUCH cheaper.

The other issue these institutions face is that there isn’t enough liquidity in the listed options to hedge themselves appropriately. Therefore, they go to one of the bulge bracket firms who sell them OTC options. (It’s also a way to make sure most of the Street doesn’t see the trades.)

When the bulge bracket broker sells these put options, they have hedge themselves…just like the dealers do with individual stocks. However, since these hedges usually involve an OTC put on the S&P 500, the broker can go out and hedge themselves buy shorting S&P futures contracts to hedge their position.

HOWEVER, since the options are way out-of-the-money, they don’t need to fully hedge them all at once. Instead, they engage in “dynamic hedging.” When they sell the put option, they merely hedge part of the contract…say 20%. If the market falls in a significant way, they’ll have to sell more futures…until they are full hedged. (This can cause some “forced selling” into a falling market.) However, as long as the market rallies…trades sideways…or only falls slightly…they don’t have to do anything. Instead, as they move into the end of the year, they slowly cover the 20% position…so that they ar flat when the OTC option expires at year-end. (They simply collect the premium (the commission) for the OTC option trade and that’s how they make their money.)

What happens, however, if the market keeps rallying in significant way??? Well, these brokers cannot gradually cover those shorts. (If the market is rallying strongly, they’ll lose more money on their short position…then they made in commissions on the trade. They don’t want to lose money, so they have to cover earlier than expected.) They have to do it earlier…and much more aggressively…than they had planned.) Yes, they’ll only have to cover a 20% position, but that can still be quite sizeable. (It’s also very likely that they are several of these position in the Street.) Therefore, the situation can feed on itself…as brokers cover their shorts and are “forced to buy” in a rising market.

We have not worked at a bulge bracket firm for many years now, so we don’t know what how much of this kind of hedging taken place this year (during the summer & fall). However, given how strong the market has been this year…and given how there are many different issues that could upset the apple cart this year…it’s a decent bet that at least some institutions have gotten involved in this kind of hedging.

Therefore, there are reasons to think that a “melt-up” could take place this year…even though there would not be any fundamental reason for such a move. (Sure the economy can improve, but the market is already pricing-in an economy that is much stronger than it is right now.)…….Thus, even though we believe that a strong correction is HIGHLY likely over the next 6-12 months, it does not preclude from a strong rally from taking place over the last 6-7 weeks of the year.

2) We have spent a lot of time discussing why we believe that the stock market is well ahead of the fundamentals in recent weeks. Despite the fact that Q3 earnings season was a good one, it is not something that belongs on the bullish side of the bull/bear ledger. Very simply, for the first time this year, we have gone through an earnings season without the forward earnings estimates on the S&P 500 being raised on the Street.

We have spent A LOT of time talking about how the stock market is well ahead of the fundamentals. (All one has to do is look at valuation levels…like the P/E ratio, price-to-sales, Case/Shiller, GDP to market cap, etc.) We have also spent a lot of time pointing out that the argument that says “growth will remain strong, so the stock market will continue to rally” doesn’t hold any water.

We all know that the central banks pushed the stock market WAY above the fundamentals in 2020…and since the stimulus has remained at emergency levels, the stock market has remained above its underlying fundamentals. In other words, as the fundamentals have improved, they have not been able to come close to fully catching up to the stock market…due to the continued emergency levels of stimulus. That stimulus/liquidity has enabled the market to stay well above anything that could be justified by the economy/earnings. (Earnings have grown just over 20% from its pre-pandemic levels…while the S&P has rallied almost 40% above its pre-pandemic levels!)

Again, there is no question that earnings beat expectations during this earning season. In fact, they beat them by a wide margin! (According to FactSet, the numbers are 13.4% above estimates vs. the 5-year average of 8.4%.) However, the consensus earnings projections around Wall Street for the full year were $200 before earnings season…and that’s what they STILL are for the full year today. The same is true for 2022 earnings…which stand at the same level they did before companies started reporting a few weeks ago. ($220 is still the consensus estimate for next year).

This is the first time this year that earnings projections have not improved during earnings season (and the improved significantly in each of the last two earnings seasons). Of course, this could change in upcoming quarters. However, when you look at the difference between the rise in PPI vs CPI, it sure looks like margins (and thus earnings) are going to have a very tough time improving as we move into 2022.

In other words, as good as the Q3 earnings have been, it sure looks like the next few quarters are not going to be as good as the past three quarters. This does not bode well for a market that is already extremely expensive…and at a time when the Fed going to taper its QE program to zero by next summer…and with the ECB indicating this past week that they’ll do the same by next fall. The Fed is going to go from adding over $1 trillion of QE stimulus in 2021…to zero…by the summer next year………We think it’s going to be very tough for the stock market to rally further without the full load of emergency stimulus…especially if earnings forecasts are not going to improve.

3) On top of the upcoming taper move by both the Fed and ECB, China has pulled-in their horns in a substantial way. We keep harping on this issue…and we’re going to keep repeated it week in and week out going forward. You can’t have the world’s second largest economy go from a decade+ of promoting leverage, debt and risking-taking…to a situation where there are clamping down on all three of these issues…without it having a noticeable impact on the global economy and the global marketplace eventually.

It’s great to hear that President Biden and China’s President Xi are going to hold a virtual summit on Monday to “confront tensions over trade, cyberthreats, the climate, Taiwan and human rights.” However, China is already saying that they don’t expect much (anything) to come out of the meetings. In fact, the Biden administration is already pushing hard to lower expectations by saying the meeting could be a tense one. (Heck, maybe President Biden will try to come off a being tough on China. It IS something he ran on…and it was certainly an issue helped former President Trump. (Heck, even some of his biggest detractors liked certain aspects of Mr. Trump’s China policy.)

In other words, there is no guarantee that we’ll see a bunch of “nicey-nice” talk about each other after these meetings. However, even if we do, the tensions between our two countries are not going to ease for very long at all. China is determined to raise their profile in the world…and the President (for life) Xi is absolutely determined to bring Taiwan fully back into the fold.

Having said all this, we do not know how soon the tensions between the two countries will grow in a significant way…or when they’ll come to a head. In fact, many experts fell that China will continue to be exceedingly patient…and that the situation will not escalate in a serious manner for a long time. However, that does not mean that other issues facing China won’t create problems for our markets over the next 12-24 months.

China has made a MAJOR shift. They have gone from promoting massive levels of risk-taking, debt and leverage…to one where they have clamped-down on all three areas in the past year. It started with Jack Ma and BABA a year ago…and it has spread through their real estate, technology, education, video gaming, gaming/casinos sectors since then.

You can’t have the world’s second largest economy go from a decade+ of promoting leverage, debt and risking-taking…to a situation where there are clamping down on all three of these issues…without it having a noticeable impact on the global economy and the global marketplace. Of course, when you combine this…with the tapering back of QE by the Fed, ECB and other global central banks…and you have a situation where elevated asset prices will become vulnerable……….We apologize for sounding like a broken record on this issue, but we strongly believe that it has to be repeated again and again.

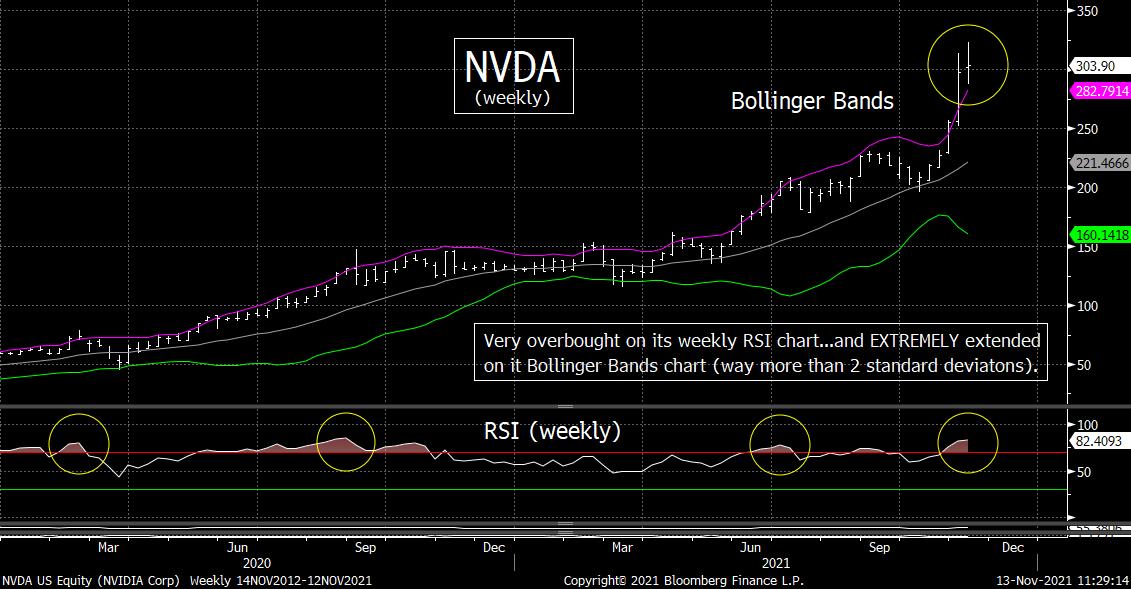

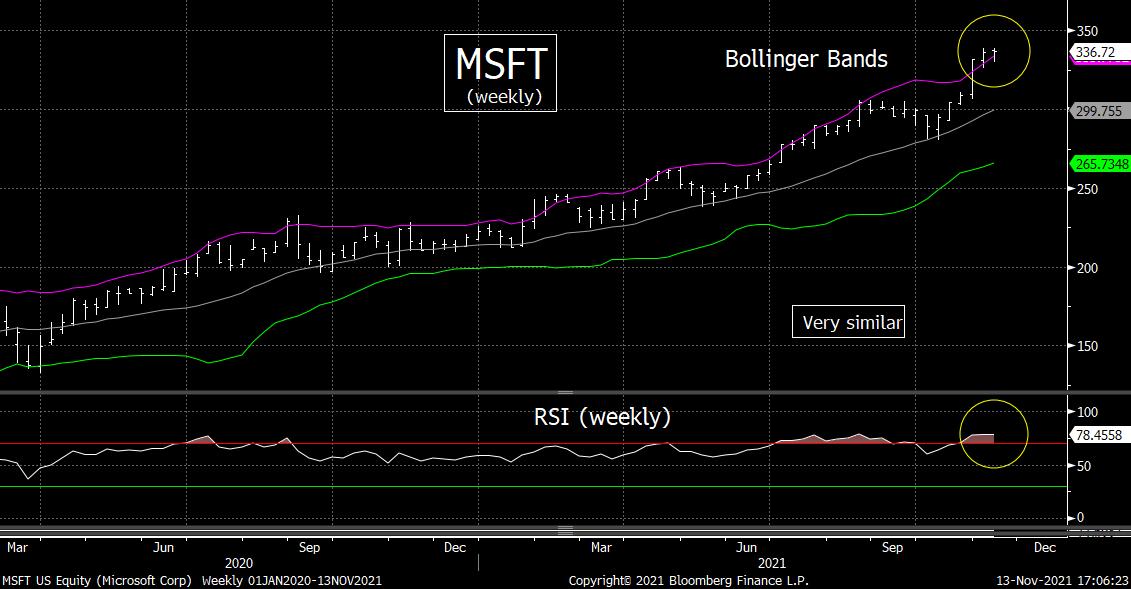

4) No stock rallies 100% of the time…even the stocks of great companies. In fact, history tells us that investors love great companies so much that they frequently push those stocks to levels that cannot be sustained on a short-term basis. Therefore, it is not unusual for the stocks of great highflying companies to see meaningful pullback/corrections more often than other stocks. Right now, we are seeing this in names like NVDA, AMD, MSFT and TSLA.

As we all know, no stock rallies 100% of the time. This is true for ALL stocks…even the stocks of the best companies in the world. It also includes the stocks of companies that change the world (and/or are in the midst of changing the world). Heck, we’d all agree that Amazon (AMZN) has changed the world over the past 25 years…and yet its stock has still seen many, many large declines. In fact, you don’t even have to go back 25 years. In just the last decade, AMZN has seen about two dozen corrections of 20%-60%!!!

Part of the reason that the stocks of these fabulous (world changing) companies rally to excessive levels is due to the fact that investors get very excited about the company’s prospects. They get SO excited that they pile into the stock without any thought of valuation. We cannot blame investors for doing this. If a company is in the midst of changing the world, the sky is the limit for their fundamentals, so it’s hard to know what their true forward valuation level should be……Also, these kinds of world changing companies gain a lot of momentum…and thus investors have confidence to add a lot of leverage to their positions.

However, the flip side of this phenomenon is that the stocks frequently get way ahead of themselves. Thus, they become vulnerable to deep pullbacks/corrections more often than many other stocks. In other words, they rally SO strongly…SO often…that they have no choice to but to experience sharp drops more often than most other stocks. (“The bigger they are the harder they fall.”)

Needless to say, just because these stocks see deep declines quite often, it does NOT mean that they cannot rally A LOT more over time. However, it DOES mean that short-term traders need to be very nimble in these names when they get extended on a technical basis (again, which happens quite frequently).

We believe that this is the situation right now with the stocks of several fabulous technology companies: TLSA, NVDA, AMD and MSFT. Actually, TSLA is one we highlighted two weeks ago…and it has already seen a sharp decline…and we think these other names have become quite vulnerable for similar declines going forward. (TSLA likely still has more downside left in it as well.)

As we highlighted two weeks ago, the RSI chart on TSLA had moved above 94! That’s the most overbought reading it has EVER seen. Therefore, it was an easy call to say that TSLA was going to fall in a significant way…and it did indeed fall 17% (20% on an intraday basis). The stock has worked off a lot of its overbought condition, but it is far from oversold…so we think it could/should still fall further. This is particularly true given that it closed well off of its highs for the day on each of the last two days. (In other words, the bounce after the sharp decline on Tuesday and Wednesday was a feeble one.)

Several other big cap tech names have also become very overbought lately…after VERY strong rallies in October. For instance, the RSI chart on Nvidia (NVDA) moved above 90 on Monday of last week. The stock did drop a little bit mid-week, but its RSI chart is still quite extended (at the 78 level). More importantly, its weekly RSI chart for NVDA still stands above the 82 level…which is a reading that has been followed by corrections in the past……On top of this, its weekly Bollinger Bands chart shows that the stock is still WELL more than 2 standard deviations above its 20-week MA.

Again, NVDA is a GREAT company…with GREAT prospects. However, it is still very overbought and thus we believe that the stock will likely see more downside movement before it sees another rally leg. Therefore, we believe investor should avoid chasing the stock at these levels. They should be able to add to positions at lower levels in the coming weeks.

The situation with AMD and MSFT is very similar. Their weekly RSI charts are overbought (AMD’s is over 80…and MSFT’s is above 78). As you can see from the weekly charts below, both of these stocks are also more than 2-standard deviations above their 20-week MA’s. (AMD’s is much more extended than MSFT’s, but their both stretched.)

None of this has anything to do with the long-term prospects of any of these stocks. They could all be trading much higher than current levels a year from now (or even six months from now). However, they all saw HUGE rallies from early October into early November. (TSLA +58%, NVDA +56%, AMD +49% and MSFT +20%.) These BIG rallies left them very overbought…and thus vulnerable to corrections that will help work-off these readings.

In fact, we would argue that a correction in these names would be normal and healthy for these stocks. It will actually give them more upside potential than if they kept rallying in a parabolic fashion. Those kinds of rallies are followed by crashes…and that’s not good for investors (or the stock market in general).

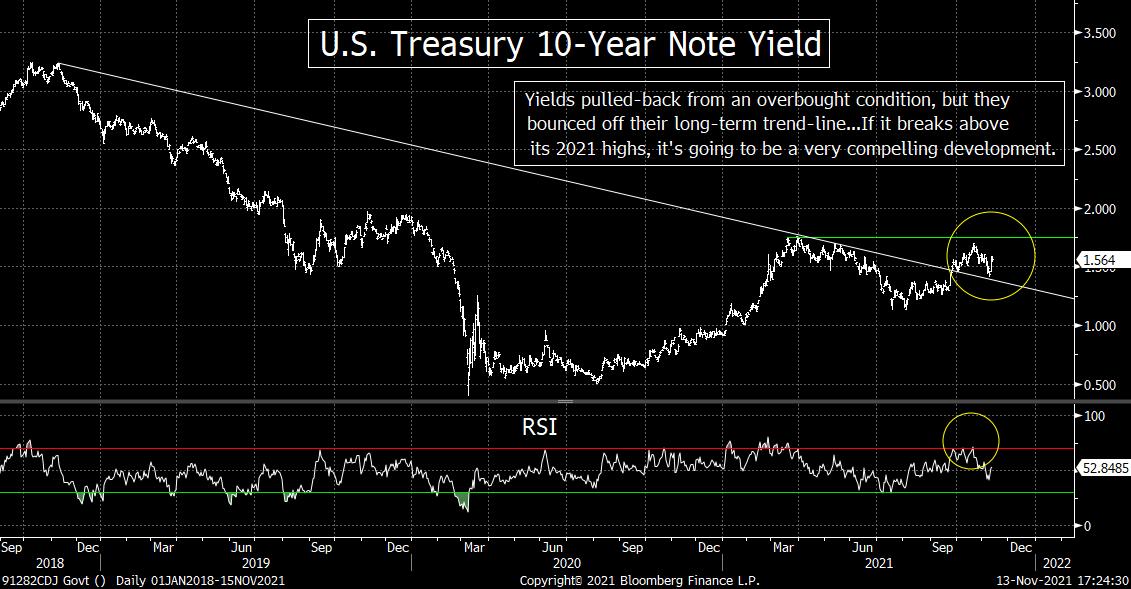

5) After a sharp pullback to work off the overbought condition it had reached in October, the yield on the U.S. 10-year Treasury note bounced strongly last week. In other words, the yield merely dropped due to technical factors in late October/early-November…and once that condition was worked-off…and we got some more fundamental news on inflation…the upward trajectory returned. Any move above the March/October highs of 1.75% in the coming weeks should have some significant implications for many different markets going forward.

The yield on the U.S. 10yr Treasury note rose above 1.7% in October…and began to flirt with the March highs of 1.75%. However, those Treasury yields became overbought in October (oversold in terms of price), so they pulled-back for a couple of weeks to work-off that condition.

Sure, there were some fundamental reasons give for this move (like the potential that Lael Brainard would be the next Fed Chair), but there were few (if any) signs that inflation is subsiding…so it was only a matter of time before the yields bounced back. The drop in the 10yr yield took it down to its multi-year trend-line, but it held that line…and bounced-back strongly this pasts week (with a lot of help from the much higher than expected PPI number).

Don’t get us wrong, there ARE signs that there is a light at the end of the tunnel when it comes to the supply chain issues. Freight costs are dropping…as can be seen by the dramatic 50% drop in the Baltic Dry Index over the past month or so. However, these supply chain issues are still going to take a long time to fix. More importantly, the MASSIVE levels of monetary and fiscal stimulus that has worked its way into the system over the past 18 months is going to keep inflation elevated for a long time to come. (The continued rise in wage pressures won’t help either.) Therefore, the inflation issue is not going to go away if/when those supply chain issues ease somewhat.

With all of this in mind…and you throw-in the “golden cross” that the 10yr yield has recently experienced…and you have a very strong case for higher long-term interest rates in the coming months. If/when they break above that key 1.75% resistance level, it’s very likely going to have an impact on today’s very expensive stock market.

6) We have spent a decent amount of time this year saying that investors should not ignore gold. It has worked as an inflation hedge for 5,000 years, so we’ve been saying that it is wrong to think that it won’t work any longer. We also said that if it broke above the $1,830 level, it will be very bullish for the yellow metal. Well, it broke above that level last week in a meaningful way.

We understand why a lot of people are looking at Bitcoin and other cryptocurrencies as a good hedge against inflation and/or a good flight to safety asset. However, we have also been saying for some time now that gold should not be ignored for the same kind of hedging.

The commodity has worked well for this purpose for over 5,000 years, so to think that it no longer has a purpose is a big mistake in our minds. In fact, we have been saying that ALL investors should be using at gold to at LEAST some degree as a hedge. Even younger people who believe whole heartedly in Bitcoin, Ethereum, etc. for many different purposes…should still use a combination of cryptos and gold in our humble opinion.

We have even more reasons this weekend to be bullish on the yellow metal. The $1,830 level had been very tough resistance for gold over the last five months. That level stopped rallies in July, August and September…and gave the commodity an “ascending triangle” pattern……..Last week’s rally ALSO took the yellow metal above its trend-line going all the way back to August of 2020!

Therefore, last week’s meaningful break above that level is very bullish for gold on a technical basis. Of course, it won’t rally in a straight line, but a push to $1,900 very quickly is the likely outcome in our opinion. After that, the $1,950 highs of late 2020 will be very reachable as well.

In other words, we remain very bullish on gold…and we want to repeat that you don’t have to be a cryptocurrency bear…to be a bull on gold.

7) The dollar made another “higher-high” in a series of “higher-lows” and “higher-highs” over many months. The DXY dollar index is getting a bit overbought near-term, but not extremely so. However, it is interesting that this dollar strength has not had an noticeably negative impact on either the commodities market or the emerging markets. In fact, there emerging markets are showing signs that they might be ready to outperform…and many months of underperformance.

The currency market has seen some big moves recently. The DXY dollar index has made a series of “higher-lows” and “higher-highs” for many months now. The thing that is interesting is that this has not had a negative impact on the commodity markets or the emerging markets.

Yes, the CRB commodity Index has flattened out over the past 3-4 weeks, but it certainly has not rolled-over…and it still stands at its highest level since 2014!......As for the EEM emerging markets ETF, the strength of the dollar has indeed caused this asset class to underperform the stock markets of the more mature economies this year. HOWEVER, even as the dollar has rallied further over the past month, the EEM has not acted as poorly as it had earlier in the year. Instead of making yet another “lower-low” in October, it bounced off its August lows. This has been followed with a “higher-low” this month…the first one since February!!!

This more recent action has taken the EEM up to the top line of a “descending triangle” pattern. Therefore, if it can rally further from here, the emerging markets asset class could fool everybody and start to outperform going into the end of the year!

Of course, we HAVE to wait for the EEM to break above this triangle pattern before we can get overly excited about this possibility. We’d also want to see it follow the recent “higher-low” with a “higher-high” (above the October highs of $52.50). However, the potential is certainly out there right now……We’d also note that the DXY dollar index is getting overbought on a short-term basis, so if it rolls-over any time soon, that could be a catalyst for the possible breakout in the EEM we’re talking about. (In fact, maybe this recent positive action in the EEM is anticipating a decline in the dollar.)

In other words, there are certainly reasons to be skeptical about a breakout in the emerging markets as we move towards the end of the year….like the slowing economy in China. However, if the EEM can rally further over the coming days and weeks, this is one asset class that could surprise everyone……..If (repeat, IF) it does breakout, it could/should have some important (positive) implications for emerging markets in 2022 as well.

8) Whenever we see a particularly large trade in the option market, it always makes us stop and say “hmmmmm.” This is especially true when the options trade is well out-of-the-money. We saw one such trade in the LQD high grade corporate bond ETF last week, so it looks like somebody is looking for a big pickup in volatility in corporate bond market over the next month or so.

Last week, a very big trade in the options market caught our eye. The trade took place on the LQD high grade corporate bond ETF. Needless to say, this is the highest quality part of the U.S. corporate bond market, so it certainly grabbed our attention.

To be specific, somebody bought 160k of the December 17th 128/131 put spread on the LQD. The buyer spent $8 million…which could provide $40 million in profits if the LQD falls to the 128 level over the next month or so…..This is not the first time we’ve seen this trade. A similar, yet smaller, trade took place in August…and another 17,000 tradeD on Friday.

The 128 level on the LQD is 4% below its current level. That might not sound like much, but it actually would be a big decline in the corporate bond market over a 4-5 week timeframe……When somebody spends a lot of money on an options trade that is well out-of-the-money, it usually means they are VERY confident that the move will take place. (They either know something…or think they know something.) That $8 million dollars can go to zero very quickly if the corporate bond market doesn’t start to fall rather quickly. Therefore, this is something that definitely made us go “hmmmmmm” last week.

If the best part of the corporate credit market sees a significant decline over the next month, it’s a good bet that the stock market will see some volatility as well. With this in mind, we’ll be keeping a VERY close eye on the LQD…the yield curve…and credit spreads…over the coming days and weeks. If some cracks form in these areas, it will raise a yellow warning flag on the stock market as well.

9) Boeing (BA) hasn’t been good stock since 2017. In fact, it hasn’t been even a decent stock since then. However, we’re starting to see signs on the technical side of things that could finally be positive for this stock. Our analysis has nothing to do with the fundamentals on BA (we do not cover the stock), so we want to provide that caveat. However, if (repeat, IF) it can rally much further from here, the stock could finally see a period of outperformance.

The pandemic has posed all sort of problems for Boeing (BA), but their problems started before anybody had ever heard of Covid-19. The debacle with their 737-Max airplane caused problems long before air travel came to a halt during the pandemic. Of course, the fact that the stock has rallied 130% off its March 2020 lows makes it seem like the stock has done well. However, the stock still stands 50% below it all-time highs from 2019. Also, since late January 2018, BA has declined 37%...while the S&P 500 has rallied 63%! So there is no question that this stock has been a bad one for quite a while.

Looking at the chart on the stock, however, it has the potential to see a period of out-performance. We do have to admit that it will take a significant further rally from here to raise a big green flag for the stock’s long-term prospects, but it won’t take much more upside movement to finally give it some nice upside momentum for a year-end rally.

The bounce in BA over the past two weeks has taken the stock up close to the top line of a ‘descending triangle” pattern, so a further rally will be bullish. However, we’d also note that the 200-DMA provided tough resistance for BA back in September and October. Therefore, if it can break above the $230 level, it will not only take it above its “descending triangle” patter, but it would ALSO take it above its 200-DMA…AND give the stock its first “higher-high” since March!

Of course, we HAVE to wait for the break above the $230 level to take place before we can confirm a change in trend for BA. However, investors might want to think about “nibbling” on the stock a

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464