Morning Comment: Bearish on Commodities, NEAR-TERM

It was a very uneventful day in the stock market yesterday...until late in the afternoon when the market gave back its earlier gains. The catalyst seemed to be comments from the “Fed Minutes” from their last meeting...which said the healthcare crisis would weigh heavily on economic activity, employment and inflation...and posed considerable risks to economic growth over the medium term.

Yes, we’re sure there has been a time when the Fed minutes have had an impact on the stock market over the past 30+ years, but we cannot remember that time. So it was strange that it caused the stock market to pull-back in that manner yesterday. That said, nobody is going to call a 0.72% drop from the morning lows a disaster, so we don’t want to make too much of this action...even with this morning’s further dip in the futures.......In other words, even though we’ve been saying that we expect a pull-back/correction soon...and the “internals” for the market have been even less impressive this week that it has been in previous weeks (with an even more “narrow” rally), we’re going to have to see a lot more downside follow-through before we can start think about raising a warning flag on the stock market.

However, before the Fed’s “minutes” hit the tape, we had already seen a big pick-up in volatility in other markets...away from the stock market. One of the most extreme outsized moves came from in the currency market...where the dollar bounced strongly and the euro experienced a significant decline. It’s too early to take a victory lap for our call for a “tradable” top in the dollar (and a similar bottom in the euro), but there’s no question that yesterday’s moves in the currency market were quite pronounced. Therefore, we believe the odds are high that yesterday’s reversal was the beginning of something that will last for more than just a few days.....In fact, given that the “positioning” and the “sentiment” on for the dollar & euro that we’ve been harping-on had reached such incredibly extreme levels early recently, we would expect any reversal in the currency markets this to last for several weeks (if not longer).

The rise in the dollar also seemed to be the main catalyst for the 2.5% declines we saw in both gold & silver, but not all commodities took it on the chin yesterday. For instance, “Dr. Copper” moved higher...and lumber shot-up another 3.3%...and the CRB commodity Index was able to rise slightly as well. However, we would expect these other commodities roll-over on a near-term basis if the dollar continues to rise over the coming days and weeks (like we believe it will).

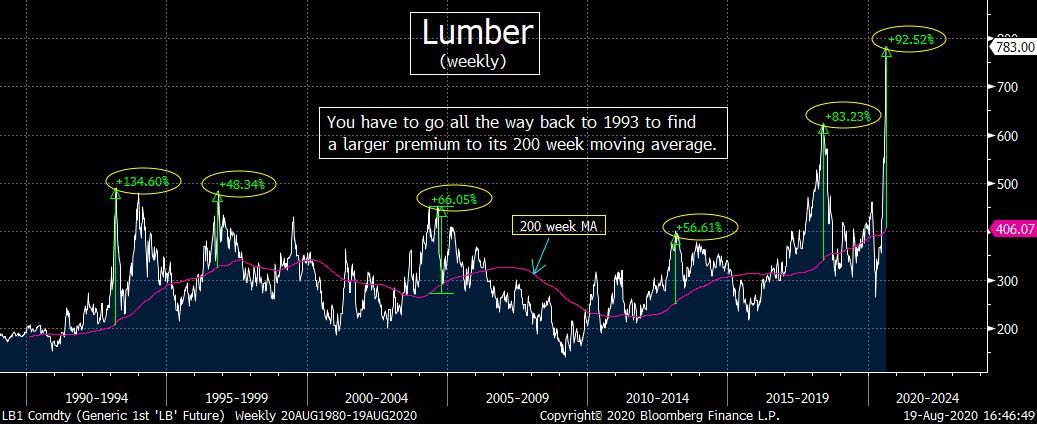

Lumber looks particularly vulnerable at these levels in our opinion...as its more than 200% rally since the April lows has gone parabolic over the last month. This has taken its weekly RSI chart (with a reading above 85) to its most overbought EVER! That’s right, our charts go back to 1984...and we cannot find another time when lumber was as overbought based on this reading!.....On top of that, this commodity also stands at a 92.5% premium to its 200 week moving average. You have to go all the way back to 1993 to see a bigger premium. So there’s no question that lumber is becoming very, very extended.

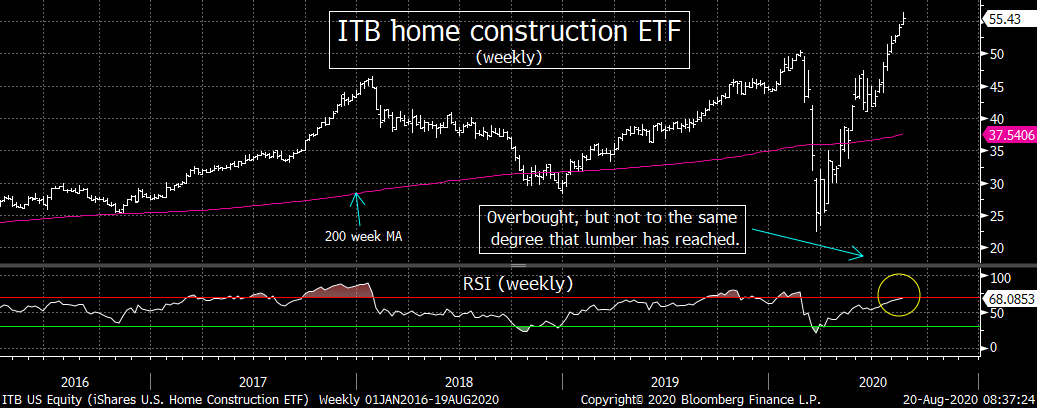

We understand why lumber prices have been rallying...and we’ve been bullish on the commodity (and housing) for quite a while. However, it has reached the kind of nose-bleed levels that make it very, very tough to rally any further over the near-term. (The housing stocks are getting overbought as well, but they have not reached the kinds of extremes that lumber has. Therefore, we would not be surprised if the housing stocks...and their ETFs...saw a pull-back soon, but the decline should not be as substantial as it will be for lumber. In other words, lumber has become SO overbought on a near-term basis that it can fall in a pronounced way without clobbering the home construction stocks in a similar manner.)

We DO want to reiterate that we are quite bullish on the commodity asset class on a longer-term basis. We just believe that the technical condition of the currency market and for many commodities...as well as the “positioning” and “sentiment” readings for both asset classes...have become so extreme that we will see the kind of reversals in these markets that will last several weeks (and therefore will become “tradable” moves).

Matthew J. Maley

Managing Director

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464