Morning Comment...Stock Poised For Another Leg Lower....June 14, 2019 - BTFNow

The last two days have been ridiculously quiet in the market place…as the composite volume has been just been just 2.47bn and 2.5bn shares on Wednesday & Thursday. Only the Friday before Memorial Day has seen lower volume all year! We did, however, get a little more movement in the market place yesterday than we saw on Wednesday…as the major averages rallied about 0.5% (and the Russell 2000 popped just over 1%)……The 4.5% bounce in oil got a lot of the credit for yesterday’s mild advance in stocks…as the stock market has had a pretty strong correlation with this commodity over the years.

However, the reason the correlation is usually a strong one is because the price of oil is frequently associated with the DEMAND. If demand is strong, the economy is strong…and thus the stock market advances along with oil. The opposite is true if demand is weak. HOWEVER, when the price of oil goes up due to an issue of too little SUPPLY (like it was during the 1970s), then the higher price of oil becomes a bearish development (as costs in the economy rise…WITHOUT a pick-up in demand). Therefore, we’re not so sure that investors should be getting excited about any rise in the price of oil that is associated with a slow-down in supply (due to issues in the Gulf).

As for the stock market, its rally has stalled-out this week, but it has not rolled-over in a compelling way….as the S&P remains above its 50 day moving average (50 DMA). However, it is becoming increasingly obvious that the market is holding up due to the expectations that the Fed will come in and buoy the market…even though the stock market weakness has only seen mild. In fact, at its worst level, the S&P was down just under 7%...and now stands less than 2% below its all time highs!!!

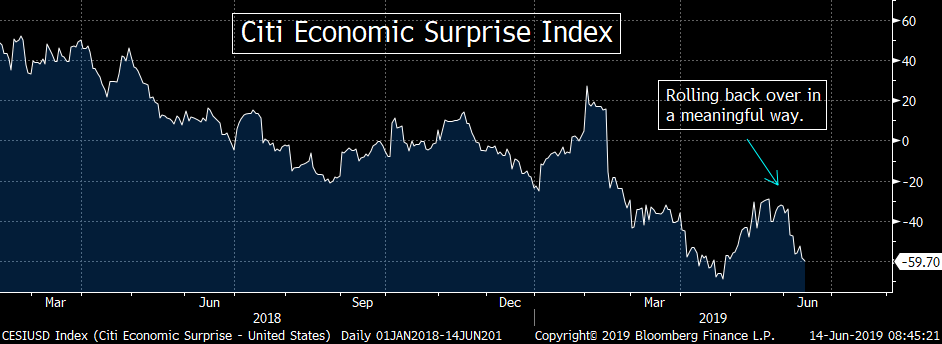

There really isn’t any other reason that would explain the way the stock market is holding up so well. The trade issue with China has not improved at all in the last week or two. If anything, the tension has only grown…with the Administration’s ultimatums towards President Xi for the upcoming G20 summit……The same is true when it comes to fundamental growth. As we have been expecting, full year earnings growth has been coming down…with more pundits following Morgan Stanley and JP Morgan’s leads by cutting 2019 S&P 500 earnings estimates this week. Similarly, we’ve seen weaker-than-expected domestic economic data (as can be seen by the rolling back over of the Citi Economic Surprise Index this month). The data from around the globe hasn’t been any better…highlighted by last night’s weaker-than-expected Industrial Production data out of China.

These are not the kind of developments that would inspire a fundamentally motivated rally. Therefore, the reason last week’s rally has held-up this week has to be due to another reason…and it seems to us that the belief that the Fed will not let the market see even a normal and healthy correction of 10% is the most likely reason. Of course, as we’ve been saying for the past two weeks, we do not agree with this assumption…but we do think it’s the one that makes the most sense to explain why the stock market has not rolled back over…yet. We just believe that the history of the past 10 years tells us that the Fed (who is at least as much “market dependent” as they are “data dependent” when it comes to their actions) will wait until the markets and the economy experience more stress than they have so for before they actually become more accommodative.

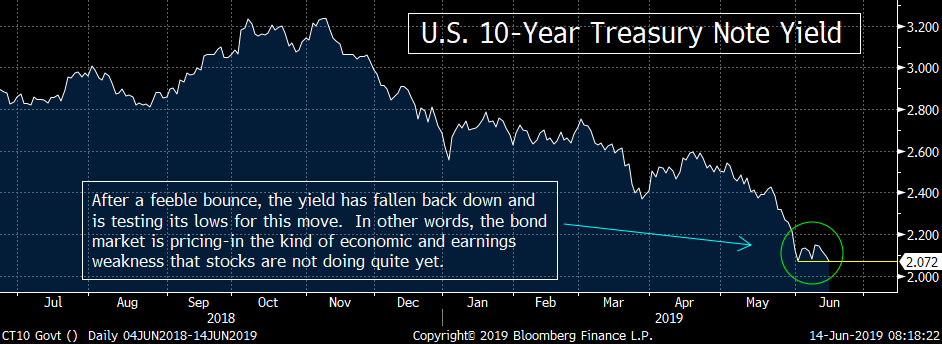

One this is for darn sure…even though the stock market has not gone back to pricing-in a weaker domestic and global economy (yet), the bond market certainly has!!! The yield on the U.S. Treasury 10-year note has fallen back down to test it late May/early June lows of 2.07% (the lows for this move). Of course, those yields could bounce-back before the day is over, but there is no question that the bond market is pricing-in the kind of weaker economy that the stock market has not done yet. In fact, it’s not even close. With the S&P 500 standing just 1.8% below its all-time highs…and with a P/E ratio at almost 19x earnings…the stock market is not pricing-in weaker growth at all. (The 19x multiple we just sighted uses “stated earnings”. The “forward P/E” is at about 17x…but given how the “E” part of the P/E ratio is declining…and could/should decline further going forward…it’s hard to use the forward P/E when trying to decide the correct valuation. Besides, 17x still isn’t cheap at all.)

We’ll finish by highlighting the disappointing earnings out of Broadcom (AVGO) last night. Their EPS number actually beat estimates slightly, but revenues fell well short…and the guidance the company gave was quite negative. In fact, not only did they lower guidance, but they said that they were seeing a broad-based slow down in demand!....This news has AVGO trading down more than 8% in pre-market trading…and very near its late May lows of $251. This, in turn, has the SMH semiconductor ETF trading lower as well. If the SMH opens where it is trading in pre-market trading right now, it will take the SMH down very close to its 200 day moving average. That 200 DMA provided excellent support in both March and May, so if the SMH breaks below that line in a significant way going forward, it’s going to be quite negative for this very important leadership group. (It saw a slight” break below that line in late May, but not a significant one. It will take a significant break below the 200 DMA to confirm the break-down.)

So it’s safe to say that we remain cautious on the stock market right here. We called for a sharp VERY-SHORT-TERM bounce in the stock market two weeks ago…and that worked very well. However, with trade negotiations with China going poorly (actually non-existent right now)…tensions with Iran increasing…and estimates for economic and earnings growth coming down…we think the early June bounce was something that only worked-off an oversold condition in the market place. Therefore, the stock market could/should roll-over soon…and begin pricing-in the weaker fundamental back-drop we are facing right now (just like the bond market has already begun doing again).

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22